Introduction

Many Quebec retirees are “house rich, cash poor.” Their paid-off homes offer little liquid income, while rising costs, healthcare, and family support strain retirement plans. Market volatility adds stress.

Reverse mortgages and home equity strategies convert property into a flexible financial resource, without requiring a sale or move. Properly used, they complement pensions, RRSP/RRIF income, and government benefits like QPP (Quebec Pension Plan) and OAS (Old Age Security). Misused, they can erode equity and harm estate plans.

As a Quebec financial planner, I help retirees compare reverse mortgages, HELOCs (Home Equity Lines of Credit), downsizing, and other tools. The goal is to support long-term retirement and tax planning, not just address short-term cash needs.

Understanding Reverse Mortgages for Quebec Retirees

Quebec reverse mortgages allow homeowners aged 55+ to borrow against home equity without mandatory monthly payments. The loan, plus interest, is typically repaid upon property sale, permanent move, or death. In 2026, significant Quebec real estate growth makes this option increasingly attractive to retirees.

Lenders usually allow access to 15–55% of home value, based on age, property type, location, and market. Since monthly payments aren’t required, interest compounds, potentially reducing inheritance. Matching the loan amount and structure (lump sum vs. installments) to a clear financial plan is essential.

Reverse mortgage funds are typically received tax-free, which benefits cash flow. However, this decision requires evaluation alongside RRSP withdrawals, TFSA room, FHSA strategies for children, and overall estate objectives.

Note that in Canada, you are required to receive Independent Legal Advice (ILA) from a lawyer or notary of your choice before signing. This ensures you fully understand the commitment and prevents any conflict of interest.

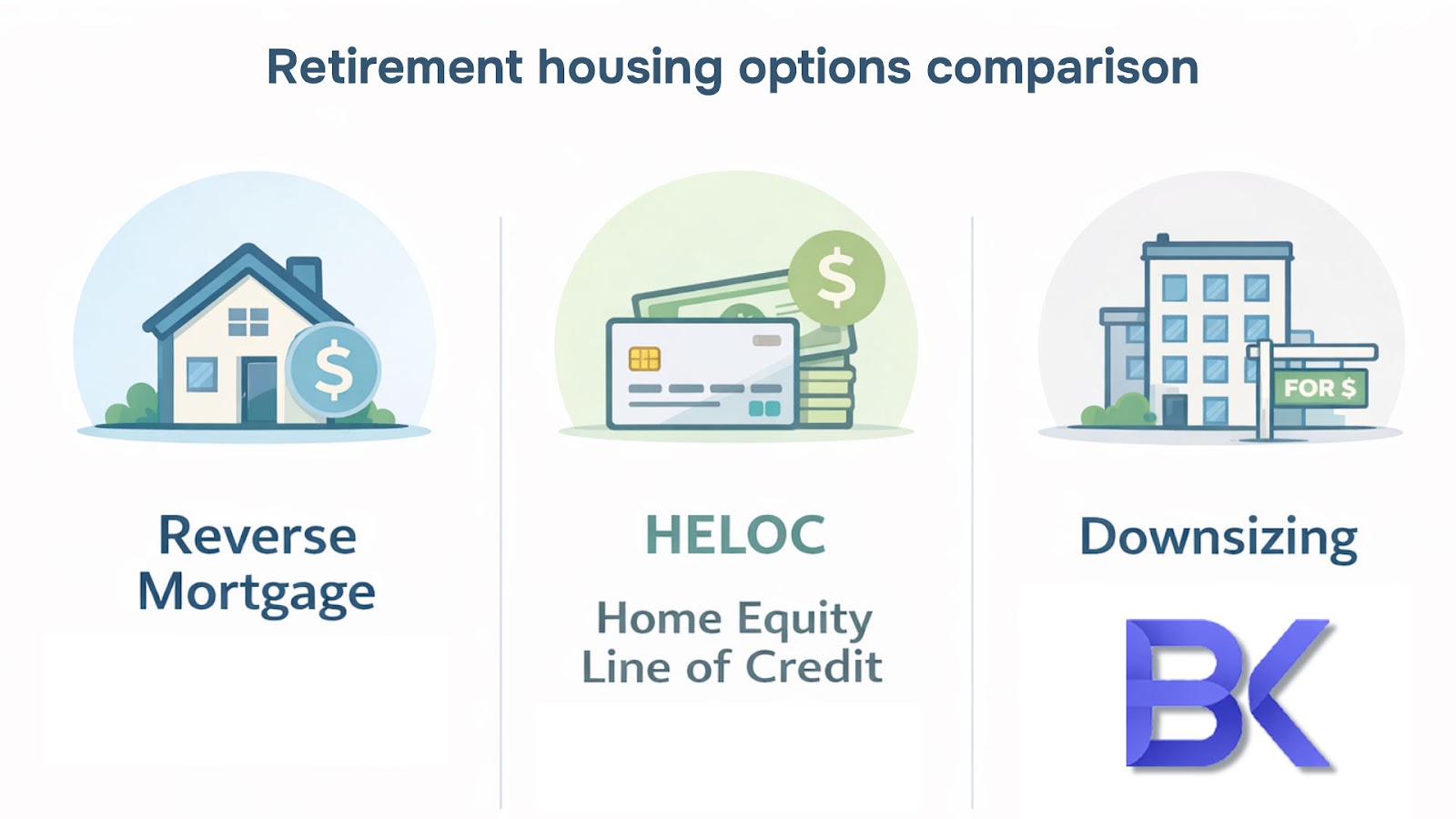

Reverse Mortgages vs. HELOCs: A Quebec Comparison

Quebec retirees often compare reverse mortgages to Home Equity Lines of Credit (HELOCs). HELOCs offer lower rates but demand regular interest payments and strong income qualification under federal rules. For retirees with defined-benefit pensions and solid credit, a HELOC can be a more flexible, cheaper option.

Modest or irregular income may prevent HELOC qualification, even with a valuable home. A reverse mortgage can be accessible then, as qualification emphasizes age and property over income. The trade-off involves higher interest and compounding debt, making careful planning crucial.

Reverse Mortgage Payout Options in Quebec

Quebec retirees can choose reverse mortgage payouts: a single lump sum, scheduled advances, or a combination. A lump sum suits major renovations, high-interest mortgage payoffs, or debt consolidation. Scheduled advances can boost monthly cash flow, acting as a private pension supplement.

These payout options carry significant tax and benefit implications. Spreading advances, for instance, can prevent large RRSP withdrawals that elevate federal and Quebec tax brackets. A clear cash-flow projection helps determine the safest payout structure.

| Strategy | When It Fits Retirees in Quebec | Main Risk/Trade-off |

| Reverse mortgage (lump sum) | Large one-time need; limited income; want to stay | Faster equity erosion; higher interest |

| Reverse mortgage (monthly) | Need regular cash-flow boost; protect GIS/OAS | Long-term compounding interest |

| HELOC | Strong income/credit; disciplined payments | Payment obligation; variable rates |

Beyond Reverse Mortgages: Quebec Home Equity Release

Quebec home equity release extends beyond reverse mortgages. It encompasses HELOCs, refinancing, downsizing, inter-family loans, and sale-leaseback arrangements. In 2026, many retirees wish to unlock property value for income and lifestyle, while remaining in their current neighbourhood.

Your home is both a residence and a significant asset. Funding retirement with home equity must prioritize secure housing, sustainable cash flow, and estate protection. Over-leveraging risks vulnerability if property taxes, condo fees, or unexpected health costs increase.

A comprehensive plan considers the current mortgage balance, age, health, desired time in the home, and family expectations. A modest reverse mortgage combined with a smaller HELOC offers flexibility for some. Others may find more secure, predictable cash by downsizing to a condo or senior residence.

Tax Planning Strategies with Home Equity in Quebec

Quebec reverse mortgage funds are not taxable income, but their use impacts your overall tax situation. Rather than making large RRIF withdrawals that increase federal and Quebec taxes and potentially reduce OAS, some retirees use home equity, maintaining lower tax brackets for registered withdrawals.

Home equity can fund strategic contributions to RRSPs for a younger spouse, TFSAs, or an FHSA for adult children’s first homes. While borrowing to invest in retirement needs caution, targeted moves with clear calculations and risk controls can enhance long-term family after-tax wealth.

Estate Planning & Protecting Heirs with Home Equity

Many Quebec retirees fear a reverse mortgage will diminish their children’s inheritance. Modern contracts typically guarantee the estate won’t owe more than the home’s fair market value upon sale, provided obligations are met. However, a large balance plus interest can significantly reduce remaining equity.

Key steps include transparency with heirs and integrating home equity strategies into wills, incapacity mandates, and life insurance planning. A life insurance policy can sometimes replace equity used via a reverse mortgage, protecting the intended legacy. Integrated financial planning is crucial for coordinating these elements, along with consumer protection rules under Canada’s Bank Act.

| Home Equity Strategy | Estate Impact | Control for Heirs |

| Reverse mortgage | Reduces equity over time | Heirs keep surplus after loan repaid |

| HELOC | Depends on use/repayment | Strong if payments kept up |

| Downsizing | Converts equity to cash | Clearer cash inheritance, smaller home |

Optimizing Mortgage Strategies for Quebec Retirees

Quebec retiree mortgage strategies go beyond rapid debt repayment. Keeping a low-rate conventional mortgage or using a reverse mortgage to clear high-interest debt can boost net cash flow and reduce risk. The decision hinges on interest rates, tax position, and retirement income mix.

Aggressively prepaying low-fixed-rate mortgages with RRSP or non-registered funds isn’t always optimal for retirees. Improving your long-term position may involve prioritizing high-interest consumer debt, restructuring obligations, and timing mortgage renewals with your retirement date.

Reverse mortgages can pay off a conventional mortgage at retirement, particularly if monthly payments are tight. This preserves your home and eliminates mandatory payments. However, it requires assessment against lifespan expectations, health, and estate values.

Cash Flow Management for Quebec Retirees

Quebec retirees manage QPP, OAS, GIS, pensions, RRSP/RRIF withdrawals, and TFSAs. Housing costs are a major budget item. Home equity can smooth cash flow and reduce anxiety, but it shouldn’t conceal unsustainable spending.

A detailed retirement cash-flow analysis reveals if a reverse mortgage is truly needed, or if adjustments to withdrawals, tax credits, or debt payments suffice. Optimizing pension start dates or shifting RRSP/TFSA assets can also create necessary financial room, without using home equity.

Risk Management & Interest Rate Considerations

Interest rate risk is key to any mortgage strategy. Reverse mortgage rates typically exceed standard fixed mortgages or HELOCs. Even with 2026 rate stability, the long retirement horizon means compounding costs can become significant.

Scenario analysis is vital: How does equity fare with modest versus stagnant home price growth? What’s your balance at age 85 or 90? Stress-testing ensures you don’t outlive your savings *and* home equity.

Integrating Home Equity into Quebec Financial Planning

Quebec retiree financial planning must integrate housing, taxes, investments, and family goals. Reverse mortgages and home equity strategies are only safe within a complete plan, accounting for longevity risk, healthcare costs, and future assisted living needs.

A robust plan begins with clear priorities: staying home, maintaining lifestyle, supporting family, and preserving estate value. Next, we quantify guaranteed income and flexible assets. Then, we decide if and how to utilize home equity.

Home equity can combine with annuities, segregated funds, or systematic non-registered withdrawals. This blend smooths income, manages taxes, and reduces the need to sell market investments during down years, benefiting risk-averse retirees.

Coordinating Home Equity with Quebec Tax Rules

Quebec’s tax system, with credits for seniors, medical expenses, and home-support services, impacts retirement income. Using home equity for in-home care or accessibility renovations can extend your time at home, leveraging provincial and federal tax credits.

Modeling various withdrawal and borrowing strategies allows comparison of after-tax results and long-term net worth. The “best” strategy often balances lifestyle, security, and legacy, rather than just maximizing short-term cash.

Key Takeaways for Quebec Retirees

- Reverse mortgages = no payments + stay home, but higher compounding interest

- HELOCs = lower rates but requires stable income/credit

- Tax-free proceeds complement RRSP/RRIF strategy

- Modern contracts*protect heirs (no negative equity guarantee)

Real Cases: Home Equity Strategies for Quebec Retirees

Case 1: Montreal couple, age 72 and 69

A Montreal couple (72, 69) owned an $850,000 duplex with a $95,000 mortgage and increasing condo expenses. Their pensions and QPP covered basics, but they felt financial pressure and worried about rising interest rates at renewal.

HELOC options failed their income stress test. Instead, a modest reverse mortgage paid off the existing mortgage and a small credit card balance. They also established a limited monthly advance for ten years. Cash flow improved by over $900 monthly, without selling the property.

Concurrently, RRIF withdrawals and TFSA contributions were adjusted to maintain a favourable tax bracket. A review of wills and life insurance ensured their children would still receive a significant estate post-loan repayment.

Case 2: Widow in Laval, age 76

A 76-year-old Laval widow owned a paid-off bungalow worth $550,000. She wished to stay home but needed funds for accessibility renovations and private homecare. Her concerns included burdening her children and reducing their inheritance.

We modeled three options: downsizing, a HELOC with interest-only payments, and a reverse mortgage with staged advances. Given her limited pension and preference for no monthly payments, a small reverse mortgage drawn in two tranches over five years was chosen.

A conservative investment portfolio was implemented, leveraging Quebec and federal tax credits for home-support services. A life insurance policy, combined with anticipated home value growth, aimed to preserve her desired inheritance.

FAQ

1. How does a reverse mortgage work for retirees in Quebec?

A reverse mortgage lets Quebec homeowners 55+ borrow against their home without monthly payments. Interest is added to the balance, which is repaid when you sell, move out permanently, or on death. The goal is to stay in your home while using part of its value to support retirement. You can check the unbiased guide on reverse mortgages by the FCAC.

2. Is a reverse mortgage better than a HELOC for Quebec retirees?

It depends on income and priorities. A HELOC usually has a lower rate but requires regular payments and strong income. A reverse mortgage is easier to qualify for and has no required monthly payments, but interest is higher and compounds, reducing equity over time.

3. Are reverse mortgage proceeds taxable in Quebec?

No. Reverse mortgage funds are generally received as tax‑free loan advances, not income. However, taking a large lump sum may influence your broader tax planning, RRSP/RRIF withdrawals, and benefits like OAS or GIS, so integrated advice is important.

4. Will my heirs lose the house if I use a reverse mortgage?

Your estate must repay the loan and interest when the property is sold. Modern contracts usually guarantee you will not owe more than the home’s fair market value. Any remaining equity after repayment goes to your heirs, but the balance between loan and value depends on how much you borrow and for how long.

5. When is downsizing better than using a reverse mortgage in Quebec?

Downsizing can be better if you are open to moving and want to lock in equity, reduce maintenance and property taxes, and possibly create a clear cash inheritance. A reverse mortgage may be better if staying in your current home is a top priority and you prefer to avoid the disruption of moving.

Ready to see whether a reverse mortgage, HELOC, or downsizing is the right fit for your Quebec retirement?

Book a personalized, no-obligation consultation to:

• Map out your retirement cash flow and tax position

• Compare home equity options with clear projections

• Understand the impact on your estate and heirs

Phone: +1-514-834-5558

Email: contact@bkfinancialservices.ca

Book Free Consultation Today – Available in English, French, Hebrew

Information current as of January 2026; rates/programs subject to change.