The First Home Savings Account (FHSA), known in Quebec as the CELIAPP, is one of the most effective tax tools for first-time homebuyers. It combines the contribution deduction of an RRSP with the tax-free withdrawal rules of a TFSA, and it is designed specifically to help you buy your first home.

For the 2025 tax year, one date is central for planning: December 31, 2025. It is the last day to make 2025 contributions and the last day to open an account if you want 2025 to count as a participation year.

With Montreal home prices now in the mid-$500k to $600k range and still rising year-over-year, first-time buyers need every advantage they can get. Enter FHSA/CELIAPP: Deduct contributions like RRSP, withdraw tax-free like TFSA – no repayment required. But miss Dec 31, 2025? Lose $8k room forever. Here’s your verified 2025 roadmap.

What the FHSA / CELIAPP Is

The FHSA is a registered account created for first-time buyers. It offers three main advantages:

- Tax-deductible contributions

- Tax-sheltered investment growth inside the account

- Tax-free withdrawals when the money is used for a qualifying first home purchase

In Quebec, the same account is called CELIAPP, but the federal rules are the same. If the home purchase never happens, the remaining funds can be transferred to an RRSP or RRIF without immediate tax and without using new RRSP contribution room. Tax will apply only when those RRSP/RRIF funds are eventually withdrawn in retirement or as regular taxable income. Non-qualifying withdrawals are taxable, so in most cases clients either buy a qualifying home or transfer the FHSA to an RRSP/RRIF by the end of the participation period.

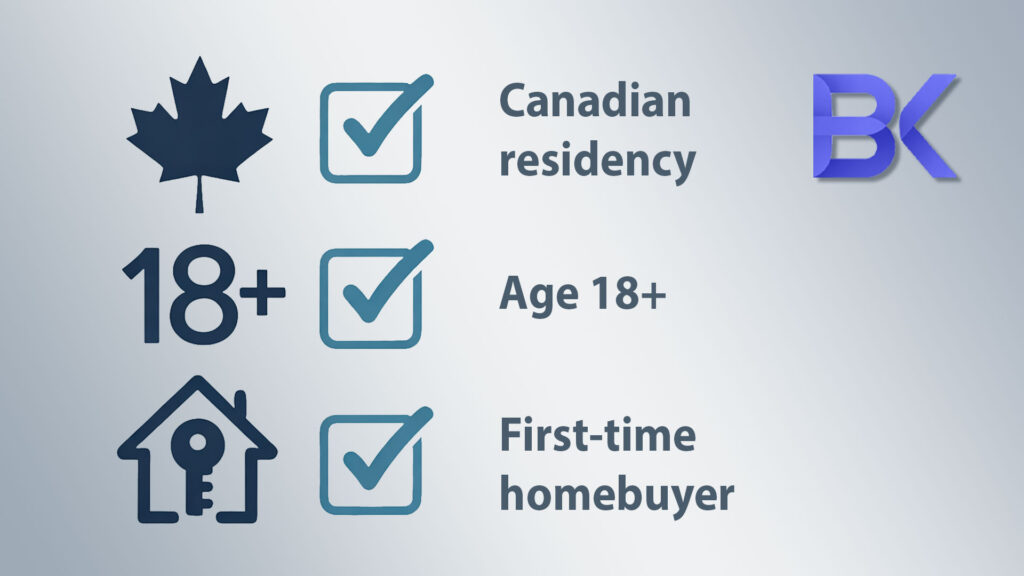

Who Qualifies

A client can open an FHSA / CELIAPP if they:

- are a resident of Canada

- are at least 18 (or the age of majority in their province)

- meet the federal “first-time home buyer” definition: they did not live in a home they or their spouse owned in the current year or any of the previous four calendar years

Revenu Québec mirrors the federal rules; claim your FHSA deduction on line 215.

For families with children, FHSA planning often runs alongside RESP planning – that’s where Quebec’s QESI incentive comes in.

There are also time and age limits that are easy to overlook:

- you cannot open an FHSA after December 31 of the year you turn 71

- your participation period ends on the earliest of:

- 15 years after you open your first FHSA

- the end of the year you turn 71

- the end of the year following your first qualifying withdrawal to buy a home

These limits matter for clients who plan far ahead or expect a longer timeline before buying.

Contribution Limits

FHSA contribution rules are simple but strict:

- Annual contribution limit: 8,000 CAD

- Lifetime contribution limit: 40,000 CAD

- Carry-forward: up to 8,000 CAD of unused annual room can be carried into a future year

- Maximum usable in a single calendar year: 16,000 CAD

For someone in a 40–50% combined federal and Quebec marginal tax bracket, an $8,000 FHSA contribution can reduce their tax bill by roughly $3,200–$4,000 compared to saving in a non-registered account.

A key point is often missed: contribution room starts only once the account is opened. Years before opening do not generate room.

Opening earlier, even with no contribution, is what unlocks your first 8,000 CAD of room.

The December 31, 2025 Contribution Deadline

FHSA contributions follow the calendar year. They do not follow the “first 60 days” rule that applies to RRSPs.

For 2025:

- Only contributions made on or before December 31, 2025 count as 2025 contributions

- Contributions made in the first 60 days of 2026 count only toward 2026

- You may choose to claim the tax deduction in 2025 or in a later year, but the contribution itself must occur in 2025 to be considered a 2025 contribution

This is crucial for clients who are used to the RRSP calendar and assume they can “top up for 2025” in early 2026. With FHSA / CELIAPP they cannot.

Why Opening the Account by December 31, 2025 Matters

Opening the account defines your first participation year and creates your first block of contribution room.

If a client opens their FHSA / CELIAPP on or before December 31, 2025:

- 2025 becomes their first participation year

- they receive 8,000 CAD of contribution room for 2025

- any unused part of that 8,000 CAD can carry forward into 2026 (up to 8,000 CAD)

Importantly, the client does not have to contribute in 2025 to lock this in. Simply opening the account before year-end is enough to generate 2025 room, which they can use later.

If they wait and open the account for the first time in 2026:

- 2025 will never be a participation year

- they permanently lose the 8,000 CAD of potential 2025 room

- the earliest year they can use room is 2026

A practical rule comes out of this:

If you want both the deduction flexibility and the carry-forward benefit, the account has to exist before the year closes.

FHSA vs RRSP vs TFSA for Quebec First-Time Buyers

When the goal is a first home, the FHSA often comes before other registered accounts, because it combines two types of advantages.

FHSA vs RRSP (Home Buyers’ Plan)

- RRSP contributions are deductible, but HBP withdrawals must be repaid over time.

- FHSA contributions are also deductible, but qualifying withdrawals for a first home do not have to be repaid.

- If the home is never purchased, FHSA assets can be moved to an RRSP/RRIF without using contribution room, and tax is deferred to future withdrawals.

FHSA vs TFSA

- TFSA withdrawals are tax-free and flexible, but TFSA contributions do not generate a tax deduction.

- FHSA gives both a deduction on the way in and a tax-free withdrawal for a qualifying home.

For many first-time buyers, this structure makes the FHSA / CELIAPP the most efficient first contribution target, before additional RRSP or TFSA funding, as long as they are reasonably sure that buying a home is part of their medium-term plan.

What Clients Should Do Before Year-End 2025

A short year-end checklist can help avoid lost room and missed deductions:

- Confirm eligibility as a first-time homebuyer under the federal definition

- Check age and timeline: opening an FHSA makes most sense if the home purchase is realistic within the 15-year window

- Open an FHSA / CELIAPP before December 31, 2025, even with a small or zero initial contribution

- Contribute any amount that you want to count as a 2025 contribution before December 31

- Keep all contribution receipts for future tax filings

- Review how the FHSA fits with RRSP, TFSA and mortgage qualification planning

For more on automating these transfers, see our 7 Habits guide. And for deduction claims, check our Quebec Tax Guide.

Quebec Buyer Pitfalls in 2025

1. Forgetting the federal first-time buyer test (current year + previous four calendar years) amid rising co-ownership trends.

2. Overlooking QPIP maternity benefits impacting home timeline.

3. Not combining with HBP – miss up to $60k + $40k FHSA = $100k down payment.

4. Waiting post-Dec 31: lose room in a volatile 2025 market, with mortgage rates still in the mid-4% range for many borrowers.

5. Ignoring French docs: CELIAPP forms available via Desjardins/Quebec notaries.

How a Financial Planner Can Help

The FHSA / CELIAPP is powerful, but it does not exist in isolation. It needs to be coordinated with:

- cash flow and emergency reserves

- existing RRSP and TFSA balances

- plans to use the RRSP Home Buyers’ Plan

- investment strategy and risk tolerance

- the realistic timing and size of a future home purchase

A financial planner can help clients:

- confirm FHSA eligibility and the right timing for opening the account

- decide how much to contribute now versus later

- choose whether to claim the deduction in the current tax year or postpone it to a higher-income year

- coordinate FHSA contributions with RRSP, TFSA and Home Buyers’ Plan strategies

- build a structured, realistic down payment plan that aligns with their broader financial goals

E.g., for an $80k earner, we might combine an $8k FHSA contribution with a $20k HBP strategy as part of building a 20% down payment on a $500k condo.

FHSA / CELIAPP vs RRSP vs TFSA: Contribution, Tax and Withdrawal Rules

| Feature | FHSA / CELIAPP | RRSP (incl. HBP) | TFSA |

| Primary purpose | Saving for a first home with tax advantages | Retirement savings, with optional HBP withdrawal | Flexible, tax-free general savings |

| Tax deduction on contributions | Yes, contributions reduce taxable income | Yes, contributions reduce taxable income | No deduction |

| Tax on investment growth | None while account is active | None while funds remain in RRSP | None |

| Tax on withdrawals | Tax-free if used for a qualifying first home | Taxable unless withdrawn via HBP (which must be repaid) | Always tax-free |

| Repayment required after withdrawal? | No | Yes, HBP withdrawals repaid over 15 years | No |

| Annual contribution limit (2025) | 8,000 CAD | 18% of income, max $32,490) | 7,000 CAD (indexed), cumulative up to $102k |

| Lifetime limit | 40,000 CAD | None | None |

| Carry-forward rules | Up to 8,000 CAD of unused room | Yes, unused room accumulates | Yes, unused room accumulates + withdrawals |

| When contribution room starts | Starts ONLY after opening the account (Year of opening) | Accumulates automatically every year | Accumulates automatically every year |

| Best suited for | First-time homebuyers seeking both deduction + tax-free withdrawal | Long-term retirement planning or HBP strategy | Emergency savings, medium-term goals, flexibility |

| If home is never purchased | Can transfer to RRSP/RRIF tax-free without using room | N/A | N/A |

Frequently Asked Questions (FAQ)

1. Do I need to contribute in 2025 if I open the FHSA this year?

No. Opening the account before December 31, 2025 is enough to generate 2025 contribution room. You can use that room in 2026 or later.

2. Can I make a 2025 FHSA contribution in January or February 2026, like RRSPs?

No. FHSA contributions count only within the calendar year. Anything contributed after December 31, 2025 is automatically a 2026 contribution.

3. What if I decide not to buy a home after saving in the FHSA?

You can transfer the full balance to an RRSP or RRIF without using contribution room and without immediate tax. Tax applies only when you withdraw from the RRSP/RRIF in the future.

4. Can I have both an FHSA and use the RRSP Home Buyers’ Plan?

Yes. These programs can be combined. Many first-time buyers use FHSA first and then supplement their down payment with an HBP withdrawal.

5. What happens to my FHSA if I turn 71 before buying a home?

Your participation must end at the end of the year you turn 71. By December 31 of that year, you must either make a qualifying withdrawal to buy a home or transfer the FHSA to an RRSP/RRIF. If you do neither and simply withdraw the money, it will be a taxable withdrawal, so in most cases the standard approach is to transfer the FHSA to an RRSP/RRIF before the participation period ends.

6. How much tax savings can I get from FHSA contributions?

It depends on your marginal tax rate. For example, someone in a 40% tax bracket who contributes 8,000 CAD may reduce their tax bill by roughly 3,200 CAD for that year.

7. Can spouses each have their own FHSA?

Yes. Each spouse can open and contribute to their own FHSA, giving a couple up to 80,000 CAD in total lifetime contributions, plus investment growth.

8. FHSA room if I opened in 2024?

$8k for 2025 auto-adds; contribute up to $16k if unused 2024 room.

9. Impact of 2025 rate cuts on FHSA?

Lower mortgage rates (~4.5%, best at this moment ~3.7-4.0) make withdrawals timelier – plan for spring 2026 buys.

10. CELIAPP for immigrants in Quebec?

Yes, if you are a Canadian tax resident in Quebec and meet the first-time buyer test; coordinate with your immigration/IRCC timelines

Don’t Lose Your 2025 FHSA Room – Act by Dec 31

Book a free 30-min audit to receive clear, practical guidance on:

- whether you qualify

- how much to contribute in 2025

- when to claim the deduction

- how to coordinate FHSA, RRSP and TFSA decisions

so you can make the most of the rules before December 31, 2025.

Speak With Boris Kolodner, MBA

Financial Planner & Licensed Financial Security Advisor (AMF/CSF)

If you want a clear, practical plan for using the FHSA or CELIAPP in 2025, you can schedule a free consultation directly with Boris Kolodner.

With more than 20 years of experience in financial planning, investments, taxation and insurance, he helps first-time buyers organize their finances, optimize contributions, and align their savings strategy with the real timeline of buying a home.

Services available in English, French, Russian and Hebrew.

Phone: 514-834-5558

Email: contact@bkfinancialservices.ca

Schedule a Free Consultation

Disclaimer: This article is for educational purposes and does not replace personalized tax or legal advice. For your specific situation, consult a professional.