In 2025, Canadians face a financial paradox. On the one hand, the government offers generous tax-supported savings programs. On the other, high interest rates and inflation are squeezing household budgets. The result: tax planning is no longer a year-end checklist but a year-round strategy that can make the difference between stability and stress.

Let’s explore the key tools that can reshape your financial future and tax planning:

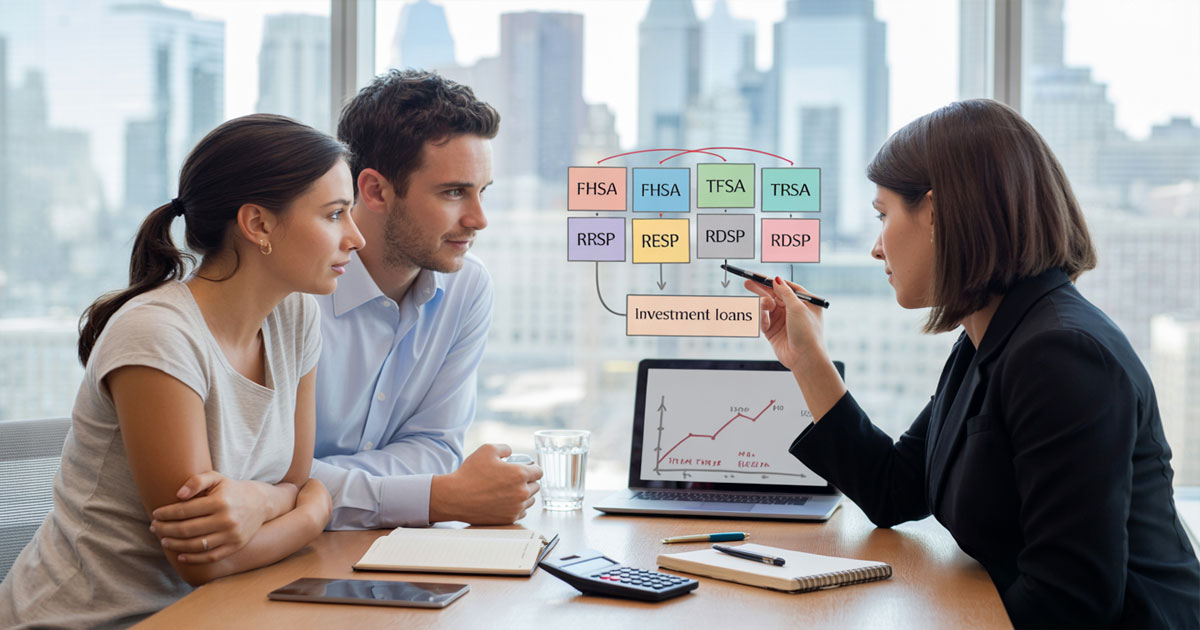

- FHSA (First Home Savings Account) – For your first home purchase.

- RRSP (Registered Retirement Savings Plan) – For retirement savings.

- TFSA (Tax-Free Savings Account) – For flexible, tax-free growth for any goal.

- RESP (Registered Education Savings Plan) – For your children’s education.

- RDSP (Registered Disability Savings Plan) – For long-term financial security for those with disabilities.

- RRSP & Investment Loans – To accelerate your savings and investments.

Used in isolation, each tool provides a clear benefit. But their real power emerges when they are understood together and applied with precision.

The Tax Levers at a Glance

- FHSA – Contributions reduce taxable income; qualified withdrawals are tax-free. A unique option lets you defer the deduction to a higher-income year.

- RRSP – The classic tool to lower your tax bill today. Contributions are tax-deductible, and investments grow tax-deferred until retirement.

- TFSA – The foundation of tax-free wealth. Contributions are made with after-tax money, but all investment growth and withdrawals are 100% tax-free.

- RESP – An investment in a child’s future. Contributions aren’t deductible, but the government adds a 20% grant (CESG). Growth is tax-deferred and taxed in the student’s hands at a low rate.

- RDSP – Powerful support for individuals with the Disability Tax Credit (DTC). Contributions are not deductible, but growth is tax-deferred, and federal grants and bonds amplify savings.

- RRSP Loans – A way to maximize your deduction now, get an immediate tax refund, and use it to pay down the loan.

- Investment Loans – Used by experienced investors to magnify returns. Interest may be tax-deductible, and only 50% of capital gains are taxed.

FHSA: Saving for Your First Home with a Double Tax Advantage

Who is it for? Canadians planning to buy their first home who want to maximize tax deductions.

The First Home Savings Account (FHSA) is Canada’s newest hybrid plan, combining the RRSP’s upfront deduction with the TFSA’s tax-free withdrawals.

- Limits and timing (2025):

- Annual limit: $8,000

- Lifetime cap: $40,000

- Carry-forward: up to $8,000 (allowing for a maximum contribution of $16,000 in a single year).

- Unique feature: You can claim the FHSA deduction in the year of contribution or defer it to a future year when your income and tax bracket is higher.

Example: A professional earns $55,000 in 2025 and expects to earn $95,000 in 2027. By contributing $8,000 in 2025 but deferring the deduction to 2027, they save nearly $1,200 more in taxes.

Combinations: FHSA withdrawals can be used alongside the Home Buyers’ Plan (HBP) from an RRSP for the same purchase.

What to keep in mind: Over-contributing incurs a 1% monthly penalty tax on the excess amount. Always check your contribution room on your CRA MyAccount.

TFSA: The Foundation for Financial Freedom

Who is it for? Every adult Canadian. It’s the most flexible and versatile savings account available.

A TFSA is perfect for building an emergency fund, saving for a car or vacation, or creating an additional tax-free income stream in retirement.

- How it works: You contribute with after-tax money. All investment growth—interest, dividends, and capital gains—and all withdrawals are completely tax-free.

- Key Advantage: Flexibility. You can withdraw money anytime without penalty, and the withdrawn amount is added back to your contribution room the following calendar year.

Example: You accumulate $20,000 in your TFSA and withdraw it for a home renovation. Next year, you can re-contribute that same $20,000 plus the new annual TFSA dollar limit.

RESP: Investing in Education with Government Help

Who is it for? Parents, grandparents, or anyone wanting to help a child fund their post-secondary education without accumulating debt.

The primary value of an RESP comes from government grants, not tax deductions.

- Canada Education Savings Grant (CESG): The government adds 20% to your contributions, up to $500 per year per child (on a $2,500 contribution). The lifetime grant limit is $7,200.

- Tax Efficiency: Funds grow tax-deferred. When the student withdraws the funds for education, the growth and grant portions are taxed in their name, typically at a very low or zero tax rate.

Example: A family contributes $2,500 per year to their child’s RESP. The government automatically adds a $500 grant. In 10 years, the grants alone will total $5,000, plus all the investment growth on top.

RDSP: Securing a Dignified Future

Who is it for? Individuals eligible for the Disability Tax Credit (DTC) and their families. This plan can be life-changing.

The power of the RDSP comes from generous government support. Even small contributions can attract significant grants and bonds.

- Grants & Bonds: The government can add up to $3,500 in matching grants and up to $1,000 in bonds annually, based on family income. The lifetime government support limit is $90,000.

- Open the Account ASAP: Even if you can’t contribute much today, opening an RDSP secures eligibility for past and future grants and bonds so they don’t go to waste.

- Tax mechanics: Contributions are not deductible, but growth is tax-sheltered. Withdrawals are taxed in the hands of the beneficiary, often at a very low tax rate.

What to keep in mind: To keep the full amount of government grants and bonds, funds should generally remain in the plan for 10 years after a contribution (the “assistance holdback” rule). Plan withdrawals carefully.

RRSP Loans: Maximizing Your Retirement Deductions

Who is it for? Individuals with unused RRSP room who want to make a lump-sum contribution before the deadline but lack the immediate cash.

- How it works: You take a loan specifically for an RRSP deposit. After filing your taxes, you use the resulting refund to immediately pay down a large portion of the loan. This gets your money compounding for retirement sooner.

Example: An engineer with $10,000 in RRSP room borrows that amount. At a 40% marginal tax rate, they receive a $4,000 refund. By applying the refund directly to the loan, the net debt drops to $6,000, while the full $10,000 is already invested.

Key Consideration: This strategy works best when the loan can be comfortably repaid within one to two years to ensure the tax benefits outweigh the interest costs.

Investment Loans: Leveraging to Build Wealth

Who is it for? Experienced investors with a stable income, a long-term horizon, and a higher risk tolerance.

Borrowing to invest (leveraged investing) can amplify gains, but it also amplifies losses.

- Tax Advantage: The interest paid on a loan used to invest for the purpose of generating income (like dividends or interest) in a non-registered account is often tax-deductible.

- Profits are often higher than 10–12%.

- Capital Gains: Only 50% of any capital gain is taxable. You can then use an RRSP contribution to offset the tax on that gain.

Example: if you realize a $20,000 gain, only $10,000 is taxable. By contributing that $10,000 into your RRSP, you can offset the tax with a deduction.

Best Practice: This is a sophisticated strategy. Ensure you have stable cash flow to service the loan, even during market downturns, to avoid being forced to sell investments at a loss.

What to keep in mind: Reviewing your investment loan each February is especially useful, since RRSP contributions made before the deadline can reduce your current year’s tax bill.

Coordinated Tax Strategies for 2025

The real efficiency comes from combining these tools:

- FHSA + RRSP (HBP) – A couple uses two FHSAs and the Home Buyers’ Plan to assemble a large down payment and buy their home years earlier.

- RDSP + TFSA – A family maximizes government grants in an RDSP for their disabled son while using a TFSA as a liquid emergency fund, protecting the long-term RDSP assets.

- Investment Loan + RRSP – A high-income earner uses an investment loan to generate capital gains, then offsets the taxable portion by contributing to their RRSP.

- RESP + TFSA – Parents use an RESP to capture all government grants for education, while saving additional funds in their own TFSAs for extra flexibility.

Mini Case Studies

- Montreal couple, age 30: Each opened an FHSA, contributing $8,000 annually. In four years, they had $64,000 plus growth. By pairing with RRSP HBP, they bought their condo two years earlier than expected.

- Single mother with disabled son: Contributed $1,500 annually to RDSP, unlocking $4,500 in annual grants and bonds. Within five years, she had built over $30,000 with only $7,500 out-of-pocket.

- Engineer in Québec, age 40: Borrowed $25,000 via an RRSP loan, applied the tax refund to reduce the balance, and gained decades of compounding. Estimated net retirement boost: $60,000 more by age 65.

- Investor with stable income: Used a $50,000 investment loan in a non-registered portfolio intended to produce income; interest fully deductible (subject to rules), lowering effective borrowing cost.

Step by Step: How to Get Started

- Check eligibility and limits – RDSP requires DTC approval; FHSA is for first-time buyers; RRSP contribution room is posted in CRA MyAccount.

- Open the accounts – Start with RDSP for government matching, then FHSA, then RRSP.

- Set up automation – Monthly contributions capture refunds and reduce the stress of lump sums.

- Decide on timing – Consider deferring FHSA deductions until your tax rate is higher.

- Document borrowing – This need will be for borrowing funds from HELOC on rental property for non-registered investment.

- Review annually – Adjust as income, goals, or tax brackets change.

Smart Planning: What to Watch For

- Over-contributing to an FHSA or RRSP, which triggers a 1% monthly penalty.

- Withdrawing from an RDSP within the 10-year holdback period, which can risk a clawback of government grants.

- Using an investment loan without stable cash flow, which could lead to forced sales at a loss.

- Taking an RRSP loan without a clear repayment plan, letting interest costs negate the tax savings.

F A Q

Can I hold both an FHSA and an RRSP at the same time?

Yes, and in many cases it’s the optimal strategy. The FHSA offers a unique mix of tax deduction and tax-free withdrawals, while the RRSP defers tax until retirement. Using both can accelerate a home purchase and build long-term retirement savings. If you never buy a home, unused FHSA funds can be transferred into your RRSP or RRIF without penalty, ensuring no tax advantage is lost. Couples who each open an FHSA effectively double their lifetime room, reaching $80,000 plus growth.

Do RDSP withdrawals affect federal benefits such as GIS or OAS?

For federal benefits, RDSP withdrawals do not reduce eligibility for Old Age Security (OAS) or the Guaranteed Income Supplement (GIS). The taxable portion of RDSP payments is excluded from the income calculations used for several federal income-tested programs and from the social benefits repayment (which includes the OAS recovery tax).

In Québec, RDSP assets are excluded when assessing eligibility for last-resort financial assistance programs. For withdrawals, Québec excludes up to $950 per month per adult when payments are structured as lifetime disability assistance payments (LDAP); larger amounts or lump-sum withdrawals may be counted and can reduce certain provincial benefits. Always confirm with your local office before withdrawing.

Are investment loans too risky for beginners?

Generally, yes. Investment loans, often called leveraged investing, magnify both gains and losses. For someone new to the market, volatility combined with loan repayments can create financial stress and emotional pressure to sell at the wrong time. These loans are better suited to experienced investors with steady income, a long horizon, and the discipline to service debt during downturns. Beginners should focus on maximizing TFSA, RRSP, or FHSA contributions first, as these offer tax advantages without leverage risk.

Do RRSP loans hurt my credit score?

Not necessarily. Reporting depends on the lender and program. Some RRSP loans aren’t reported to credit bureaus (generally with terms up to 2 years), while others are reported like any installment loan. Terms can range from 1–10 years. Paying on time helps build your history; late/missed payments will hurt your score. A common approach is to use the tax refund from the RRSP contribution to immediately reduce the balance, lowering interest costs and credit exposure. (Availability and reporting policies vary by lender; suitability depends on your cash flow and timeline.)

Can family members contribute to my FHSA or RDSP?

For the FHSA, only the account holder can make official contributions. That said, family members can gift money to the holder, who then deposits it into the FHSA and claims the tax deduction. For the RDSP, anyone can contribute with written permission from the plan holder, and the government grants still apply as long as the beneficiary is eligible.

What happens if I over-contribute to an FHSA or RRSP?

CRA charges a penalty tax of 1% per month on the excess amount until it is withdrawn. Over-contributions are one of the most common mistakes with registered accounts. Always track contribution room through CRA’s MyAccount portal before depositing large amounts, especially if you hold multiple accounts across different institutions.

Can I combine an FHSA with the Home Buyers’ Plan (HBP)?

Yes. The CRA allows Canadians to use both for the same qualifying home purchase. This means you could withdraw up to $40,000 (plus growth) from your FHSA and up to $60,000 under the HBP from your RRSP, creating a much larger down payment. The main difference: FHSA withdrawals are tax free, while HBP withdrawals must be repaid to your RRSP over 15 years.

Which is better: a TFSA or an RRSP? It depends on your income and goals.

- An RRSP is better if you are in a higher tax bracket now than you expect to be in retirement. The upfront tax deduction provides significant savings today.

- A TFSA is better if you are in a lower tax bracket now, as you won’t benefit as much from a tax deduction. It’s also superior if you need flexibility, as all withdrawals are tax-free and don’t affect government benefits. For many Canadians, the best strategy involves contributing to both.

If I withdraw money from my TFSA, do I lose the contribution room? No, and this is a key feature of the TFSA. The full amount you withdraw in a calendar year is added back to your contribution room on January 1st of the following year. For example, if you withdraw $10,000 in 2025, you can re-contribute that $10,000 in 2026, in addition to the new annual limit for 2026.

What happens to the money in an RESP if my child doesn’t pursue post-secondary education? You have several options, so the money is never lost.

- Keep the plan open: An RESP can remain open for up to 36 years, giving the child time to decide.

- Transfer to a sibling: The funds can be transferred to a sibling’s RESP.

- Close the plan: You always get your original contributions back, tax-free. The government grants (CESG) are returned to the government. The investment growth can be withdrawn or, more effectively, up to $50,000 can be transferred tax-deferred to your RRSP (or your spouse’s RRSP) if you have contribution room.

How much should I contribute to an RESP to get the maximum government grant? To maximize the basic Canada Education Savings Grant (CESG), you should aim to contribute $2,500 per child per year. This will trigger the maximum annual grant of $500 (20% of your contribution). If you’ve missed previous years, you may be able to make catch-up contributions to claim unused grant room.

Plan Ahead, Cut Your Taxes, Build Your Future

The FHSA, RRSP, TFSA, RESP, RDSP, and investment loans are not just savings tools; they are powerful components of your financial strategy. Used wisely, they lower today’s tax bill, accelerate long-term growth, and protect your family’s security.

At Boris Kolodner Financial Services, I help clients across Canada design plans that fit their income, lifestyle, and goals—not just the rules on paper.

📞 Call: 514-834-5558

📧 Email: contact@bkfinancialservices.ca

💻 Schedule a free online consultation today

With the right guidance, you can turn complex programs into a clear path toward financial independence.