Many Quebec parents wish to save for their child’s education, but RESP rules, government grants, and timing can be confusing. Too many families delay their Registered Education Savings Plan (RESP) contributions until the end of the year. This procrastination often leads to budget stress in December and increases the likelihood of missing out on thousands of dollars in free government grants.

A simple automation strategy makes saving easier and vastly more efficient. In Quebec, June is often a practical time to set up recurring contributions because tax season is behind you, spring refunds may have arrived, and it is easier to choose a sustainable monthly amount. The QESI is paid once a year, and the exact deposit timing can vary by provider and processing cycle.

If you are reviewing your cash flow or long-term financial planning in Quebec, understanding how RESP contributions interact with CESG and QESI is the key to building a smarter, stress-free routine.

Saving for Education in Quebec: RESP Basics

An RESP is a registered tax-advantaged account designed to help you save for a child’s post-secondary education. The lifetime RESP contribution limit is $50,000 per child. However, the true power of the RESP lies in the government incentives available to Quebec families.

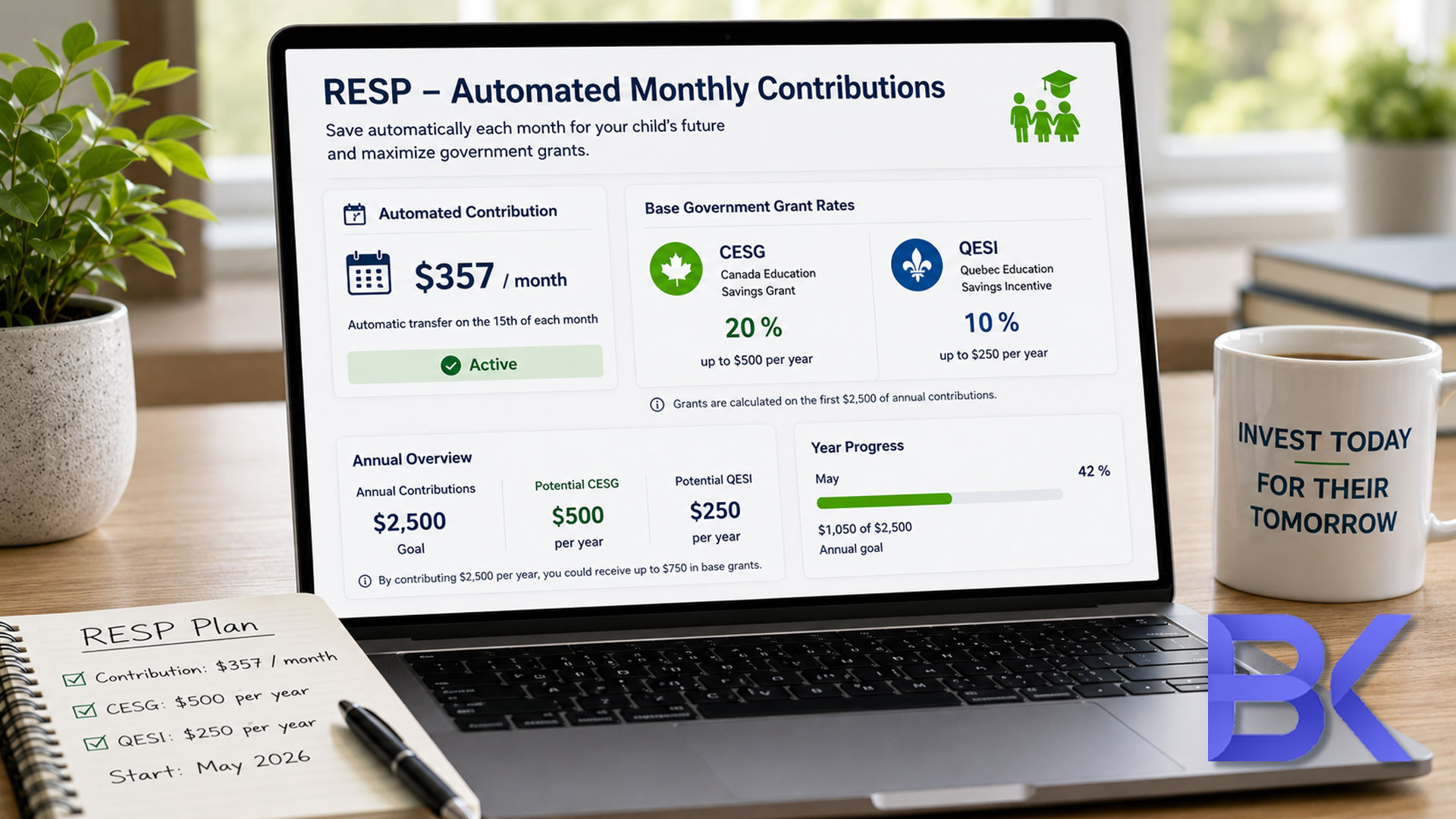

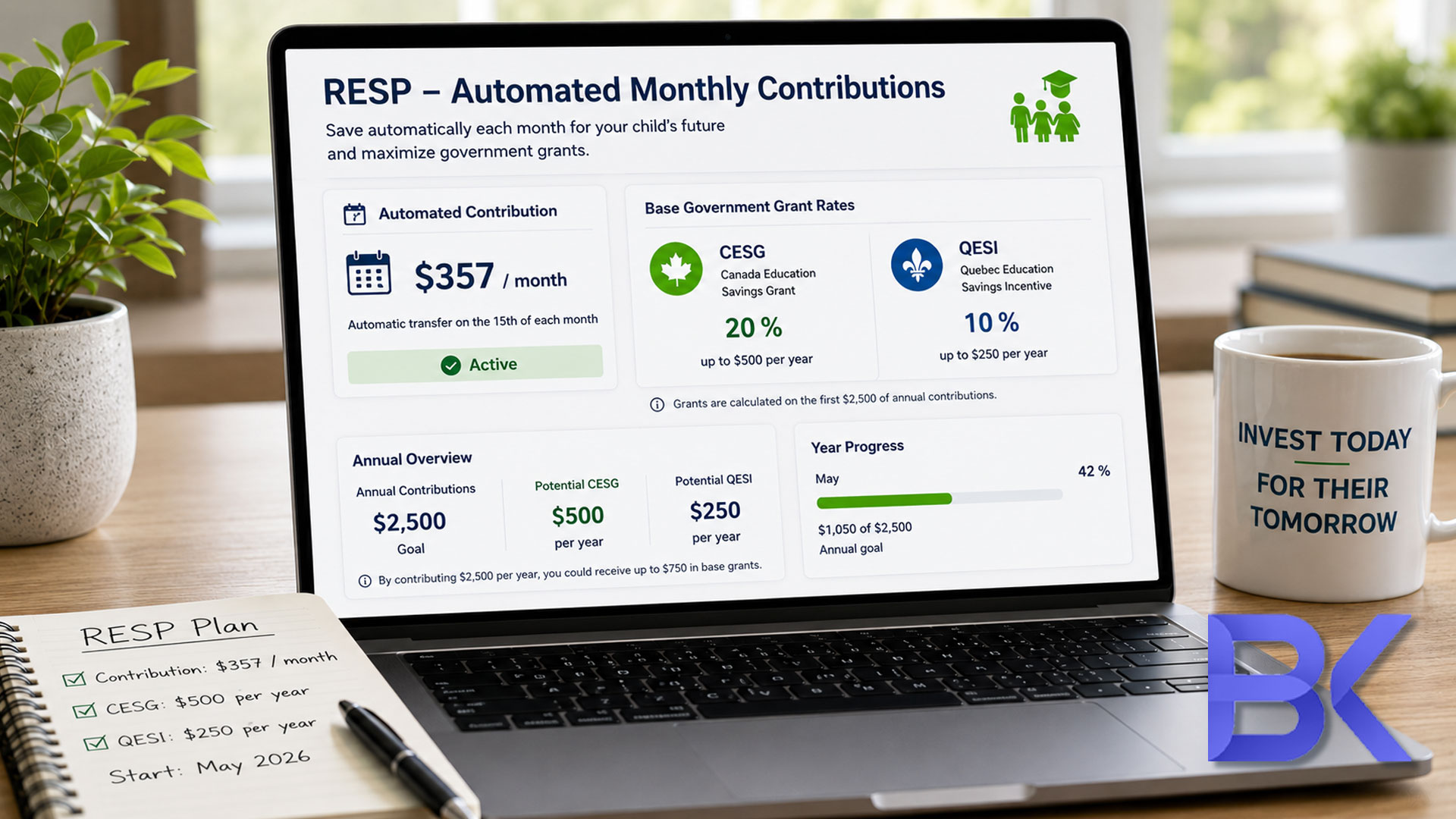

- CESG: Eligible contributions qualify for federal CESG grants, which provide a 20% match on your annual eligible contributions (up to $500 per year).

- QESI: Quebec’s QESI program provides additional provincial education savings incentives, adding a basic 10% match up to $250 per year, with possible additional amounts depending on family income, for eligible Quebec residents..

June is the perfect mid-year checkpoint for automation. After filing taxes, households have a clear picture of their net income and updated budgets, making it much easier to choose a sustainable monthly contribution amount.

Planning for the CESG (Federal Grant)

To maximize the standard grants, a family needs to contribute $2,500 annually per child, which unlocks the full $500 federal match and $250 provincial match. Spreading this $2,500 over monthly transfers starting in June (roughly $357/month for the remaining 7 months) is far more manageable than scrambling to find a lump sum during the expensive December holiday season.

Automation completely removes decision fatigue. Consistency is the mathematical secret to compounding education savings over 18 years.

QESI Timing Strategy: The June Advantage

The Quebec Education Savings Incentive (QESI) adds a compelling psychological reason to start right now. Revenu Québec typically deposits QESI funds for the previous year into RESP accounts in late May or early June.

Seeing that free provincial money hit your child's account right now is the ultimate motivation to automate your deposits for the current year. For parents with irregular cash flow, starting in June allows you to spread out payments before year-end, successfully funding a plan that might otherwise be neglected.

When to Start RESP Automation in Quebec:

| Start Time | Contribution Approach | Likely Benefit |

| January | 12 monthly deposits | Full‑year discipline and the smoothest cash flow. |

| June (Mid-Year) | 7 monthly deposits | The perfect practical restart after tax season refunds arrive. |

| December | Lump sum only | High risk of missed planning, budget stress, and lost grants. |

CESG's Impact on Your RESP

The CESG is often the primary reason families open an RESP. It rewards your eligible contributions with immediate federal assistance. Delaying your contributions means delaying the tax-advantaged growth of that free money within the account.

June is a highly beneficial time to act because it follows a major financial checkpoint. After filing taxes and settling spring budgets, parents know exactly where their financial standing is.

Instead of viewing education savings as an afterthought at the end of the year, families can use the start of summer to set a recurring transfer that fits their actual net income. This proactive approach feels significantly more sustainable than stressing over a massive lump-sum promise in December.

Grant Catch-Up Rules for Older Children

If you missed contributing in prior years, do not panic. Catch-up rules allow you to recover unused grant room gradually. Families can carry forward unused CESG room and may be able to receive up to $1,000 of CESG in a single year if enough carryforward room is available and the beneficiary meets the age rules.

Consistent planning is crucial for parents of older children. A delayed start does not mean a lost opportunity, but waiting further only narrows your available window to claim this free money before the child turns 17.

Monthly vs. Lump-Sum Funding

While a lump sum works for households with massive cash flow, monthly automation is universally more practical. It smooths budgeting and helps self-employed individuals contribute without strain.

For young families in Quebec facing rising costs like daycare, groceries, and property taxes, a manageable pre-set transfer is the only realistic way to maintain long-term education goals without sacrificing daily needs.

QESI: Quebec's Education Savings Boost

The QESI offers Quebec families an additional layer of provincial support, making education planning here particularly lucrative when done early and systematically.

Because this provincial incentive is strictly tied to eligible RESP contributions, missing a year means permanently losing out on valuable investment growth time. June helps families recover their savings momentum after a busy first quarter. It allows you to build a rock-solid automated routine just before heavy summer vacation spending begins to drain your cash flow.

Parents who automate mid-year consistently find that saving becomes effortless, drastically reducing the risk of inconsistent funding patterns.

Mid-Year Eligible Child and Account Review

A mid-year check-in is also the perfect time for confirming beneficiary information, family plan structures, and banking details. Administrative issues or mismatched SINs can completely delay government grants, so catching them now keeps your free money on track.

This review is especially critical for blended families, newcomers to Quebec who are navigating the Canadian tax system for the first time, or parents opening a family plan for multiple children.

Coordinating with Your Household Budget

Education savings must fit into your broader financial ecosystem. If a family is aggressively paying down high-interest debt or restructuring a summer family budget, the RESP amount must be realistic.

Start with a smaller automated amount if necessary. Contributing $50 a month is infinitely better than doing nothing and missing another year of compounding grants entirely. You can always increase the automated amount later when your income grows.

Family Situation vs. Mid-Year Action

| Family Situation | Action to Take This June | Education Savings Effect |

| New parents | Open account and automate | Builds the habit early and maximizes 18 years of grants. |

| School‑age child | Add recurring deposits | Removes budget pressure before the Q4 holiday season. |

| Older child (missed years) | Review catch‑up options | Maximizes the remaining grant window before age 17. |

Financial Planning in Quebec for Education Goals

RESP decisions should never be made in a vacuum; they must align with your overall financial planning. A holistic approach helps you determine realistic contribution amounts, prioritize high-interest debt repayment, and seamlessly fit RESP savings alongside your RRSP, FHSA, and long-term retirement planning.

Reviewing Contribution Limits: While maximizing grants is the goal, overcontributing can create an overcontribution tax, so families should track both contribution room and grant targets carefully. Families must carefully track their annual grant targets against the strict $50,000 lifetime contribution cap per child. A professional review ensures an efficient, error-free contribution pattern.

At BK Financial Services, Boris Kolodner, MBA, Financial Planner and Financial Security Advisor, assists Quebec families in aligning these crucial education goals with their real cash flow. With over 20 years of experience, he helps clients coordinate RESP contributions alongside mortgage obligations, emergency reserves, and retirement objectives.

June serves as the ideal reset point. Tax documents are completely current, refunds have landed in bank accounts, and parents can easily build a winning contribution strategy before the second half of the year becomes too busy.

Using Tax Refunds Wisely

Many savvy families practice a "hybrid" funding method in June. They allocate a portion of their spring tax refund as a lump sum to initiate the RESP deposits, and then set up a smaller automated monthly transfer for the rest of the year.

This is a brilliant way of using your tax refund wisely. It creates immediate momentum and drastically reduces the monthly cash flow needed for the rest of the year to reach the $2,500 target.

Real Quebec Cases: Education Savings Grants in Action

Families often understand the value of grants in theory, but implementation fails due to a lack of structure. Here are two common Quebec financial planning scenarios.

Case 1: Young Family with Uneven Cash Flow

A Montreal couple with two children wanted to save for school but postponed RESP deposits. Daily expenses always took priority, and they never had $5,000 lying around for year-end contributions. Result: After tax season, we reviewed their cash flow in early June. We set up automatic $150 bi-weekly transfers aligned with their paydays. They began qualifying for the maximum grants regularly, removed the stress of remembering, and created a sustainable wealth-building habit.

Case 2: Late Start with Catch-Up Pressure

A self-employed parent in Laval opened an RESP account but made inconsistent contributions for years. They worried about lost time and missing the government match. Result: We reviewed their remaining carry-forward grant room, created a structured catch-up schedule, and automated deposits starting in June aligned with their business income. The client regained control, successfully captured the backlog of grants, and avoided the year-end scramble that caused their prior delays.

FAQ

1. Why is June a great time to automate RESP contributions in Quebec?

June follows tax season, meaning you have a clear view of your net income and refunds. It is also the time when Revenu Québec deposits last year's QESI grants, making it the perfect psychological checkpoint to automate your savings for the rest of the year.

2. Can I still get CESG if I start contributing later in the year?

Yes, eligible contributions made later in the year still qualify. However, waiting increases the chance of forgetting or failing to find the cash. Automation guarantees you hit your target.

3. Are RESP grants like CESG and QESI automatically applied?

The CESG is generally deposited automatically within a month or two of your contribution. The QESI, however, is calculated annually and deposited by Revenu Québec into the RESP typically in the spring/early summer of the following year. Learn more about RESP account setup in Quebec.

4. How much should I contribute to an RESP each month?

To maximize the standard grants without catch-up room, you need $2,500 annually per child (about $208/month). However, a realistic amount of $50 or $100 a month is always better than an aggressive target you are forced to cancel.

5. Should I prioritize RESP contributions over debt repayment?

It depends on the interest rates. High-interest credit card debt (19%+) should almost always be cleared first. However, if you only have a low-rate mortgage, the guaranteed 30% return (20% federal + 10% provincial) from RESP grants usually outweighs the cost of low-interest debt.

Stop Leaving Free Government Money on the Table

RESP planning works best when education savings fit realistically within your broader financial strategy. At BK Financial Services, Boris Kolodner, MBA, helps Quebec families coordinate RESP contributions, maximize CESG and QESI eligibility, and align education funding with retirement and mortgage goals.

Don't wait until December. Let's automate your wealth-building strategy today.

Schedule a Free Consultation:

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

(Available in English, French, Russian, and Hebrew. With over 20+ years of experience, we help you avoid overcommitment while efficiently using available grants.)

Disclaimer: This article is provided for general informational and educational purposes only and should not be interpreted as individualized financial, investment, tax, legal, or accounting advice. RESP rules, CESG and QESI eligibility, contribution limits, and government programs are subject to change. Financial planning strategies should always be evaluated based on your personal financial situation and risk tolerance. Consult a qualified financial professional before making decisions.