Many Quebecers spend decades diligently saving into their RRSPs, only to postpone withdrawal planning until the mandatory deadline approaches. This procrastination severely limits your financial flexibility and often leads to higher taxable income later in retirement.

By law, your RRSP must be closed by the end of the year you turn 71. Poor timing and a lack of strategy can lead to larger mandatory withdrawals, which may push you into higher tax brackets and increase the risk of benefit clawbacks.

Early planning makes the transition from a Registered Retirement Savings Plan (RRSP) to a Registered Retirement Income Fund (RRIF) much smoother. A smart withdrawal strategy, pension income splitting, and careful tax coordination can drastically reduce your lifetime taxes and maximize the money left in your pocket.

In Quebec, this planning is especially crucial due to our unique combined federal and provincial tax rules. Retirees must navigate QPP income, high provincial tax rates, and the interaction between private withdrawals and government benefit eligibility.

Early Planning for RRSP to RRIF Tax Savings

While the annual RRSP contribution deadline gets all the media attention, the real long-term financial value lies in efficiently drawing down those registered savings. RRSPs offer fantastic tax-deferred growth, but eventually, every dollar withdrawn becomes fully taxable income – either directly from the RRSP or later via a RRIF.

Holding a large RRSP balance at age 71 can create a trade-off: it provides continued tax-deferred growth, but it also leads to larger mandatory RRIF minimum withdrawals. This forced income may push you into a higher tax bracket precisely when you don't need the extra cash. In Quebec, this can mean higher combined federal and provincial taxes, and it may also affect income-tested benefits such as OAS.

Timing Your RRSP Withdrawals (The "Meltdown" Strategy)

Early RRSP withdrawals can be highly beneficial. Taking modest, planned withdrawals during your lower-income years (e.g., between retiring at 62 and turning 71) can purposefully reduce your future RRIF balances. This "meltdown" strategy smooths out your taxes over time, preventing a larger tax bill in your 70s.

Key RRSP Maturity Deadline

You are legally required to convert your RRSP by December 31 of the year you turn 71. Your options include transferring the funds to a RRIF, buying an annuity, or cashing it out entirely (generally not tax-efficient due to immediate, massive taxation). Most Quebec retirees opt for a RRIF due to its investment flexibility.

| Age/Stage | Planning Focus | Tax Goal |

| 55-64 | Estimate retirement income sources | Build a multi-year withdrawal plan |

| 65-70 | Consider partial RRSP drawdown | Reduce later mandatory RRIF minimums |

| 71 | Convert to RRIF before the deadline | Avoid rushed, penalized tax decisions |

RRIF Implications for Quebec Retirees

A RRIF maintains your tax-deferred investment growth but forces you to make minimum annual withdrawals. The required withdrawal percentage increases as you age. If you retire with a substantial RRSP, these mandatory payments might far exceed your actual daily spending needs.

This can materially ruin retirement income efficiency for Quebec retirees who also receive employer pensions, QPP, Old Age Security (OAS), rental income, or dividends. Stacking forced RRIF income on top of these sources can easily bump you into a 40%+ marginal tax bracket.

RRIF Withholding Tax Considerations

It is important to note that while minimum RRIF withdrawals don't automatically trigger withholding tax at the source, any extra withdrawals do. However, withholding tax is merely a prepayment to the government. It does not represent your final tax bill. You may still owe additional tax when filing your federal and Quebec returns in April if your overall income is high.

Navigating the Quebec Tax Landscape

Quebec retirees must consider more than just basic withdrawal rules. RRIF withdrawals are taxed as ordinary income. This income, combined with other retirement cash flow, can have a significant impact.

For 2026 planning, consider marginal tax rates, OAS recovery risk, age amount eligibility, and how registered withdrawals affect family net income. This is especially vital for couples coordinating retirement income.

Quebec Tax Brackets and RRIF Income

The tax cost of RRIF income depends on your total taxable income. Even a small additional withdrawal can push some income into a higher tax bracket, especially with existing pension, QPP, and investment income.

OAS Clawback (Recovery Tax) Risk

If your total net retirement income exceeds the annual Old Age Security (OAS) recovery threshold (which adjusts annually), your OAS benefits will be clawed back by the government. For higher-income retirees, a coordinated RRSP drawdown before age 71 shrinks future RRIF minimums, directly mitigating this OAS clawback risk in your later years.

| Strategy | Short-Term Effect | Long-Term Tax Benefit |

| Delay all withdrawals to 71 | Lower tax now | Massive future RRIF income & higher taxes |

| Partial withdrawals at 65-70 | Pay some tax now | Smoother, lower lifetime taxation |

| Split eligible pension income | Better family tax balance | Lower combined household tax bill |

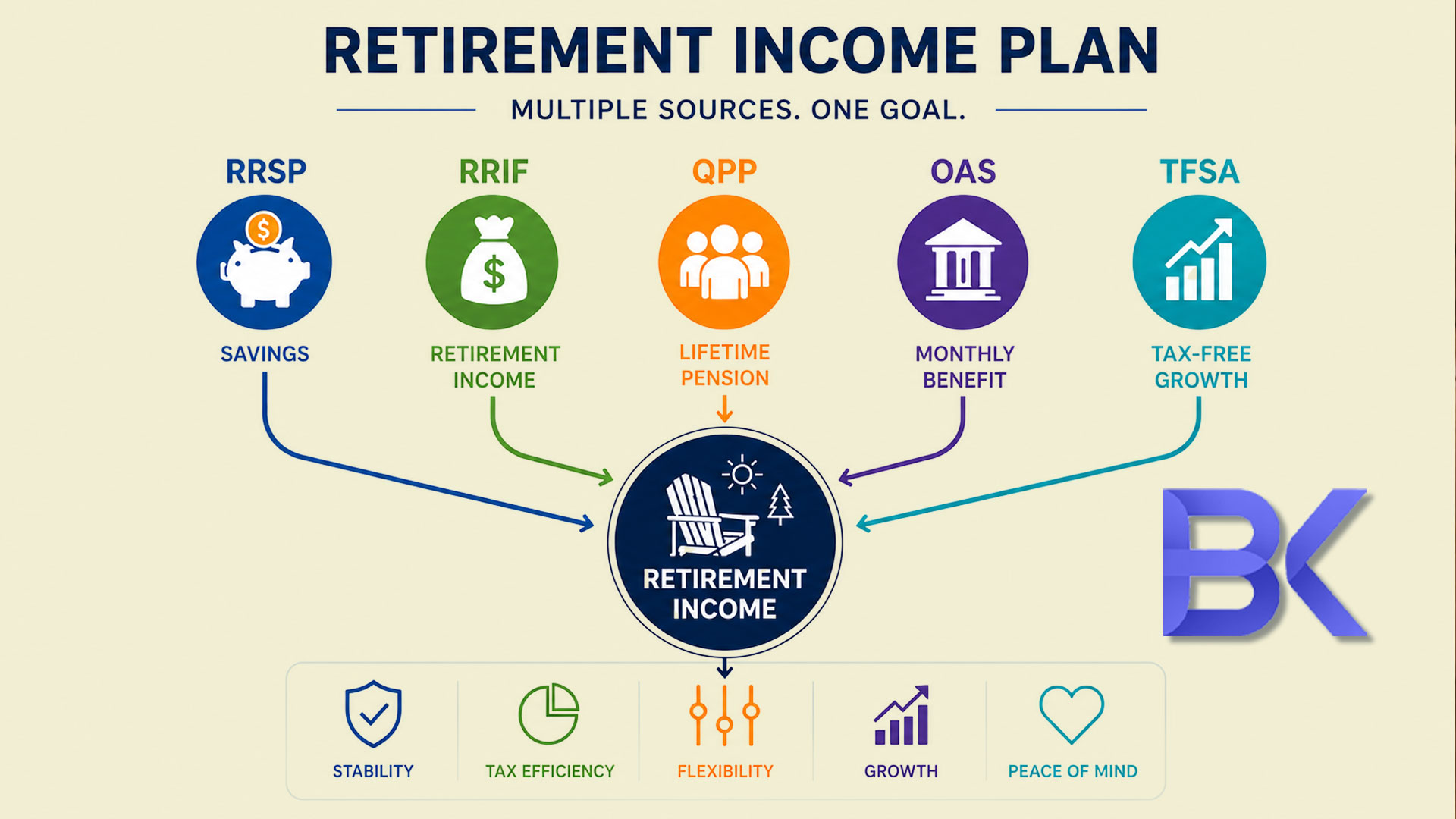

Comprehensive Retirement Planning

RRSP to RRIF planning cannot be done in isolation. It involves determining when to take income, from which accounts, and in what sequence.

A frequent, costly error is using RRIF withdrawals only after non-registered income sources have been drained. Many Quebec households benefit from multi-year projections that carefully align RRSP/RRIF income with tax-free TFSA assets, pensions, and debt obligations.

Spousal Planning for Retirement Income

If one spouse holds the vast majority of the retirement savings in their RRSP, future RRIF withdrawals will create a highly disproportionate tax burden.

Expert Tip: Starting at age 65, RRIF withdrawals generally qualify as eligible pension income, which may allow you to split up to 50% of that income with your spouse or common-law partner on your tax return. This strategy can drop the higher-earning spouse into a lower tax bracket, which can reduce household tax payable.

Estate Considerations for RRIF Planning

A large RRIF can pose a massive tax challenge for an estate. When you pass away, the remaining RRIF balance is generally taxable in your final return unless it can roll over tax-deferred to a qualifying spouse or common-law partner, or another designated transfer applies.

Proper early conversion planning involves naming a "qualifying survivor" (like a spouse) as the beneficiary, allowing the RRIF to roll over to them tax-deferred, helping preserve more of the estate for your family.

2 Real Cases: Decumulation in Action

Case 1: Retiring at 66 with a massive registered balance

- Situation: A Quebec professional planned to delay accessing their $800,000 RRSP until age 71, living off non-registered savings until then.

- The Problem: Projections showed that at age 72, their mandatory RRIF minimums, combined with QPP and OAS, would trigger the highest tax brackets and completely claw back their OAS benefits.

- The Solution: We developed a "meltdown" strategy, drawing $40,000 annually from the RRSP between ages 66 and 70. This resulted in a significantly smaller RRIF at age 71, more stable annual taxable income, preserved their OAS, and provided highly predictable retirement cash flow.

Case 2: A couple with heavily uneven savings

- Situation: One spouse held $600,000 in an RRSP, while the other had very limited registered assets. Without planning, future RRIF income would have created a severely imbalanced tax burden.

- The Solution: BK Financial developed a coordinated strategy utilizing Spousal RRSPs leading up to retirement, and implemented aggressive pension income splitting once the primary earner turned 65. The couple dramatically improved their household net income and lowered their projected lifetime taxes by thousands of dollars.

FAQ

1. When must I convert my RRSP to a RRIF in Quebec?

You must convert your RRSP by December 31 of the year you turn 71. This is a strict federal rule that applies equally to Quebec residents.

2. At what age can I split my RRIF income with my spouse to save on taxes?

In Canada, you must be 65 years of age or older to split your RRIF income with your spouse or common-law partner on your tax returns.

3. Are RRIF withdrawals taxable in Quebec?

Yes. RRIF withdrawals are considered ordinary, fully taxable income for both federal and Quebec provincial tax purposes.

4. How can I reduce taxes when moving from RRSP to RRIF?

Plan structured withdrawals before age 71, aggressively coordinate income sources (TFSA vs. RRIF), split income with your spouse after 65, and manage your OAS clawback risk. A customized multi-year plan is the only way to effectively minimize your lifetime tax burden.

5. Is a RRIF better than just cashing out the RRSP as a lump sum?

Almost always, yes. A RRIF allows your investments to continue growing tax-deferred, and you only pay tax on the amounts you withdraw each year. Cashing out an RRSP as a large lump sum will trigger an immediate, massive tax bill, which can create a very large immediate tax bill, depending on the amount withdrawn and the retiree’s other income.

Stop Giving Your Retirement Savings Back to the Government

Converting an RRSP to a RRIF shouldn't be a panicked, last-minute decision made at age 71. It requires a precise, multi-year "decumulation" strategy to ensure you keep the money you spent decades saving.

Boris Kolodner, MBA, helps Quebec retirees, professionals, business owners, and families coordinate RRSP withdrawals, RRIF planning, retirement cash flow, and long-term tax efficiency. With over 20 years of experience, we help you avoid hasty decisions and build a practical income plan.

Schedule a Free Retirement Planning Discussion Today:

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

(Consultations available in English, French, Russian, and Hebrew)

Disclaimer: This article is provided for general informational and educational purposes only and should not be considered individualized financial, tax, legal, investment, or retirement planning advice. RRSP, RRIF, pension, OAS, and tax rules are subject to change. Retirement income strategies should be evaluated based on your specific objectives, income sources, family structure, and risk tolerance. Consult a qualified financial professional before making financial decisions.