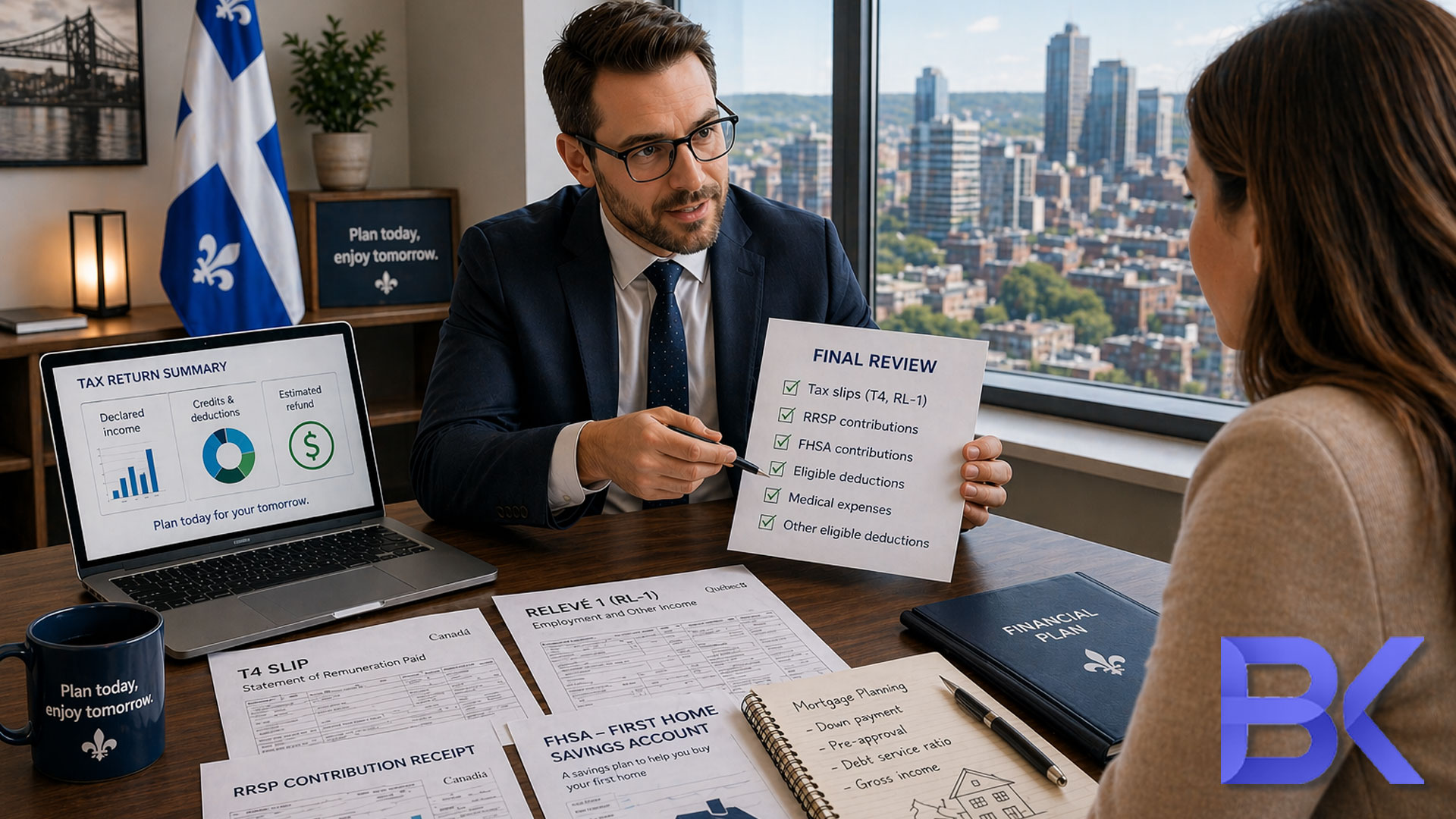

The Final Review: Quebec and Federal Details

Before submitting your return, ensure it accurately reflects figures for both the Canada Revenue Agency (CRA) and Revenu Québec. Digital filing is the fastest method, but it doesn’t replace a thorough final human check.

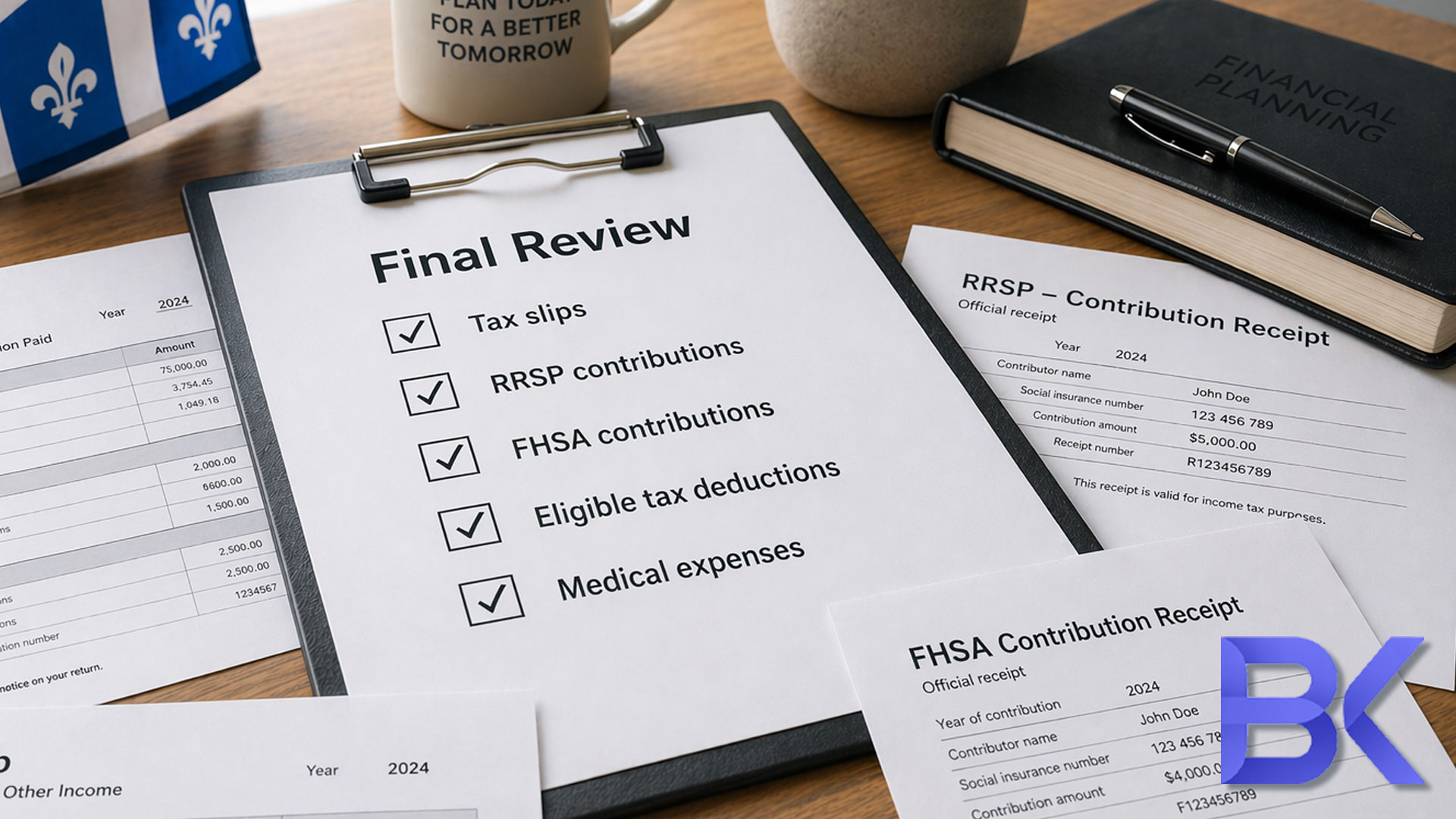

Verify your personal details: name, address, SIN, marital status, Quebec residency, direct deposit information, and dependents. Errors here can significantly delay your refunds or benefit payments.

Confirm all tax slips are included. Review your T4, T4A, T5, RL-1, RL-3, RL-24, pension statements, investment income records, and any side hustle documentation. If you are unsure what to look for, consult our detailed guide on checking T-slips and RL-slips.

Federal and Provincial Slip Matching

Quebec taxpayers receive both federal and provincial slips. Ensure the income amounts on your return match these slips precisely, especially for employment, pension, and investment income, as minor discrepancies can trigger automated reviews.

Net Income Accuracy Check

Your net income impacts many credits and benefits. Missing or incorrect slips can alter your eligibility for child benefits, the GST/HST credit, and provincial support programs.

| Final review item | Why it matters | What to check |

| Personal details | Prevents processing delays | SIN, address, marital status |

| Income slips | Avoids reassessment | T4, RL-1, T5, RL-3, T4A |

| Direct deposit | Speeds up refund | Banking information on file |

Optimizing RRSP Deductions Before You File

RRSP contributions are a key last-minute review item for Quebec taxpayers. If you contributed in the first 60 days of the year (before the March deadline) for the prior tax year, verify that it is reported correctly in your software. Your critical decision now is whether to deduct all or only a part of it.

Contribution Room Review

Compare your RRSP receipts to your Notice of Assessment and available deduction room via CRA My Account. This is crucial for those with bonuses or year-end self-employed contributions.

Over-claiming causes immediate compliance issues; under-claiming leaves immediate tax savings unused.

Deduction Timing Strategy

You don’t always need to deduct an RRSP contribution immediately. Strategic timing can improve tax efficiency if you anticipate a higher tax bracket later.

An RRSP deduction is most valuable if your income was higher than usual. If your income was lower this past year, consider reporting the contribution but carrying the deduction forward to a future, higher-earning year.

Confirming FHSA Contributions and Deductions

The First Home Savings Account (FHSA) is vital for Quebec first-time homebuyers. Before hitting “submit”, confirm your contributions, unused room, and ensure the correct FHSA deduction is entered.

The FHSA offers tax relief now and potential tax-free withdrawals later. Correct reporting is essential, especially if you are planning to apply for a mortgage in Quebec soon.

Review your official receipts and contribution dates. If you opened the FHSA but didn’t maximize it, note the remaining room to optimize your savings for future years.

First-Home Planning Review

If you plan to buy soon, align your tax return with your home-buying strategy. Review your FHSA, RRSP, cash flow, and debt obligations together before purchasing.

Deduction Coordination

If you contributed to both an FHSA and RRSP, ensure combined deductions fit your income planning. A balanced approach can boost savings without sacrificing future flexibility.

| Deduction item | Filing question | Review point |

| RRSP | Claimed or carried forward? | Contribution room and timing |

| FHSA | Entered correctly? | Receipt, annual limit, future home plan |

| Other deductions | Fully documented? | Receipts and eligibility |

Last-Minute Checks for Overlooked Tax Deductions

Many returns are filed with the correct income but incorrect deductions. Before April 30, review all potential deductions, especially if your work, family, or housing situation changed recently.

- Employees: Verify deductible expenses (ensure you have your signed T2200).

- Self-employed: Review home office, auto logs, phone, internet, supplies, and professional fees.

- Families: Double-check childcare costs (RL-24), medical expenses, support payments, and moving expenses.

- Students, newcomers, and young professionals may miss deductions. A brief final review often identifies valuable, overlooked items.

Medical and Family Claims

Claim medical expenses if they exceed the relevant threshold and meet eligibility rules. Families should also verify childcare amounts and Quebec-specific credits.

If you are part of a couple, it is usually mathematically better for the lower-income spouse to claim the medical expenses.

Self-Employed Expense Review

If you freelance or run a business, reconcile income and expenses. Ensure business expenses are reasonable, documented, and separate from personal spending.

How Tax Filing Impacts Your Financial and Mortgage Planning

A tax return is more than just government compliance; it is a financial planning checkpoint impacting your retirement savings, debt reduction, and cash flow.

For instance, your tax return heavily influences mortgage planning, particularly if you are self-employed, newly employed, or looking to buy property. Lenders scrutinize declared income, consistency, and documentation.

For many Quebec households, tax filing is also time to review paycheque withholding, retirement planning, and savings targets. It reveals if your current strategy supports or hinders long-term goals.

Ensure your reported income supports your financing goals before filing. While aggressive business write-offs reduce your taxes today, they directly lower your qualifying income for a mortgage tomorrow. A technically correct tax return might still need strategic adjustments if home ownership is your near-term goal. To dive deeper into this, read our guide on home-buying strategies for Quebec residents.

Handling Your Refund or Balance Owing

If you are expecting a refund, decide its use beforehand so the money doesn’t evaporate into daily spending. Options include paying high-interest debt, building an emergency fund, or investing it.

If you owe money, create an immediate payment plan. Missing the April 30 filing deadline will trigger a 5% late-filing penalty plus daily interest from both the CRA and Revenu Québec. Always file on time, even if you cannot pay the full balance immediately.

Mortgage Planning in Quebec

Your tax return influences mortgage planning, particularly if self-employed, newly employed, or buying property. Lenders examine declared income, consistency, and documentation.

Ensure your reported income supports your financing goals before filing. Aggressive write-offs reduce taxes but may lower mortgage qualification income in Quebec.

Coordinate tax filing with overall financial planning. A technically correct return might still need strategic adjustments if home ownership is a near-term goal.

Income Presentation for Financing

Employees should confirm T4 and RL-1 accuracy. Self-employed applicants must ensure business income is documented. Clean records simplify financing discussions.

Home-Buying Timeline

If buying within 12-24 months, your filing choices matter. Consider FHSA, debt ratios, reported income, and down payment strategy before submission.

2 Real Cases

Case 1: A young Montreal professional planned a quick filing using only their T4 slip. During a final review, we uncovered an RRSP receipt from the first 60 days of the year and consolidated eligible medical expenses. This drastically increased their refund, directly supporting their savings for a future condo.

Case 2: A self-employed Quebec client intended to claim massive business deductions without considering their mortgage timing. A coordinated review adjusted the return to stay tax-compliant while supporting a higher qualifying income for their upcoming mortgage renewal, reducing both tax-time and banking surprises.

FAQ

What is the most important review item for a Quebec tax return?

Prioritize matching your income slips, verifying personal information, and confirming deductions. Then, strategically review your RRSP, FHSA, family credits, and self-employed amounts.

Can I still reduce my taxes before the Quebec April 30 deadline?

By late April, most deductions rely on prior contributions or spending (since RRSP and FHSA deadlines have passed). However, a meticulous final review helps you correctly claim overlooked deductions and optimize how you apply them to maximize your refund.

Do Quebec taxpayers need to check both federal and provincial tax details?

Yes. Quebec residents file both federal and provincial returns, making slip matching (like comparing your T4 to your RL-1) and data accuracy absolutely essential to avoid processing delays.

Should I claim my RRSP deduction this year or carry it forward in Quebec?

Consider your current and expected future income. If you expect to jump into a significantly higher tax bracket next year, carrying the deduction forward will yield a larger tax return in the future.

How does my Quebec tax return impact a mortgage application?

Lenders use your reported net income to determine your borrowing capacity. Your filing choices, especially regarding business write-offs if you are self-employed, directly affect how much a bank will lend you.

Don’t Leave Your Money on the Table!

With the April 30 deadline just days away, a minor oversight can lead to missed refunds or unnecessary CRA penalties. Let me give your return a strategic final review. We will ensure your RRSP, FHSA, and all eligible deductions are correctly claimed to maximize your tax savings.

Book Your Free Consultation Today!

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

Available in English, French, Russian, and Hebrew. Reach out now to secure your tax savings before the deadline!

Disclaimer: This article is provided for general informational purposes only and does not constitute personalized financial, tax, or legal advice. Tax laws, deduction rules, and filing deadlines (such as the April 30 deadline for personal tax returns) are strictly enforced by the CRA and Revenu Québec and are subject to change. Always consult with a qualified financial planner or tax professional to evaluate your specific situation before filing your tax return.