Many Quebec taxpayers rush February RRSP contributions to reduce their tax bill. This haste often leads to avoidable mistakes, costing them refunds today and retirement income tomorrow.

With over 20 years of Quebec financial planning and tax experience, I often hear, “I just put money in my RRSP… I hope I did it right.” This guide shows how to avoid common February RRSP contribution errors and turn deadline stress into a clear strategy.

We’ll cover contribution limits, Quebec tax impacts, RRSP vs. TFSA vs. FHSA decisions, and how to coordinate RRSPs with mortgages, debts, and long-term retirement planning.

Understanding the Quebec RRSP Contribution Deadline

A common pitfall is misunderstanding the RRSP contribution deadline for tax purposes. For the 2025 tax year, the deadline is March 2, 2026.

Under Canadian tax law, if the March 1 deadline falls on a weekend, it is pushed to the next business day, not backward to February. Since March 1, 2026, is a Sunday, the official deadline for the 2025 tax year is Monday, March 2, 2026.

Many Quebec residents wrongly assume any February contribution is “good tax planning.”

CRA data shows most annual RRSP deposits occur in the two weeks before the deadline. Rushing often leads to guessing your room, ignoring your marginal tax rate, and choosing the wrong account. Always verify your RRSP room on your CRA My Account and latest Notice of Assessment before moving funds.

Verifying Your Official RRSP Contribution Room

Using your bank’s estimated “contribution room” instead of CRA data is a frequent mistake. Bank apps can be outdated or incorrect. Overcontributions exceeding the $2,000 lifetime buffer can incur a 1% monthly penalty from CRA.

Always confirm your official RRSP deduction limit on your latest Notice of Assessment and in CRA My Account. This is crucial, especially after job changes, bonuses, or RRSP pension adjustments.

Navigating RRSP Deadline Year vs. Tax Year for Quebec Deductions

Another common error is assuming a February 2026 contribution can only apply to the 2026 tax year. In reality, you can claim the deduction in the contribution year or carry forward any unused portion to future years.

If you anticipate a significantly higher tax bracket next year (e.g., promotion, business income growth, property sale), contribute before the deadline but carry forward the deduction. This can boost your combined Quebec and federal tax savings substantially.

Common February RRSP rush errors vs. better approach

| February RRSP Habit | Risk / Mistake | Better Practice |

| “Whatever I can afford before deadline” | Random amount, unused room, poor cash flow | Plan monthly/bi-weekly contributions year-round |

| Trusting bank app room | Possible overcontribution penalty | Use CRA My Account + Notice of Assessment only |

| Claiming full deduction immediately | Lower tax refund in future higher-income year | Strategically carry forward some deductions |

| Using RRSP for short-term savings | Forced withdrawals, taxes + withholding | Use high-interest savings or TFSA for short-term goals |

Maximizing Quebec Tax Savings: Beyond Just the Refund

Many Quebec residents focus solely on the "How big will my refund be?" question when making February RRSP contributions. This approach can lead to choices that appear good in April but harm long-term net worth.

Combined federal and Quebec marginal tax rates can reach 37%–53% for higher earners in 2026. RRSPs are powerful in these brackets, but only if coordinated with other deductions (union dues, childcare, investment interest) and your spouse’s income.

For example, at a combined marginal rate of around 37%, a $5,000 RRSP contribution can generate roughly $1,850 in tax savings. At a 45% combined rate, the same $5,000 contribution can produce about $2,250 in tax savings.

Why Overprioritizing Refund Size Can Be Costly

Chasing the biggest refund without considering real net income over time is a mistake. For example, using a 19% interest line of credit for a last-minute RRSP deposit to gain a 37% tax saving is usually a poor trade-off. The after-tax refund rarely offsets ongoing high-interest debt costs.

A better strategy involves first clearing high-interest debt, then planning RRSP contributions that align with your budget, mortgage, and retirement timeline. The optimal mix might include RRSP, TFSA, and even FHSA for first-time Quebec homebuyers.

Leveraging Spousal RRSPs for Family Tax Efficiency

Another refund-focused error is contributing only to your own RRSP when a spousal RRSP could reduce your couple’s lifetime tax bill. If you earn more than your spouse, directing some February contributions to a spousal RRSP helps balance retirement income and avoids future pension splitting issues.

This strategy is especially valuable for young couples where one spouse takes parental leave or for families running small businesses with uneven incomes.

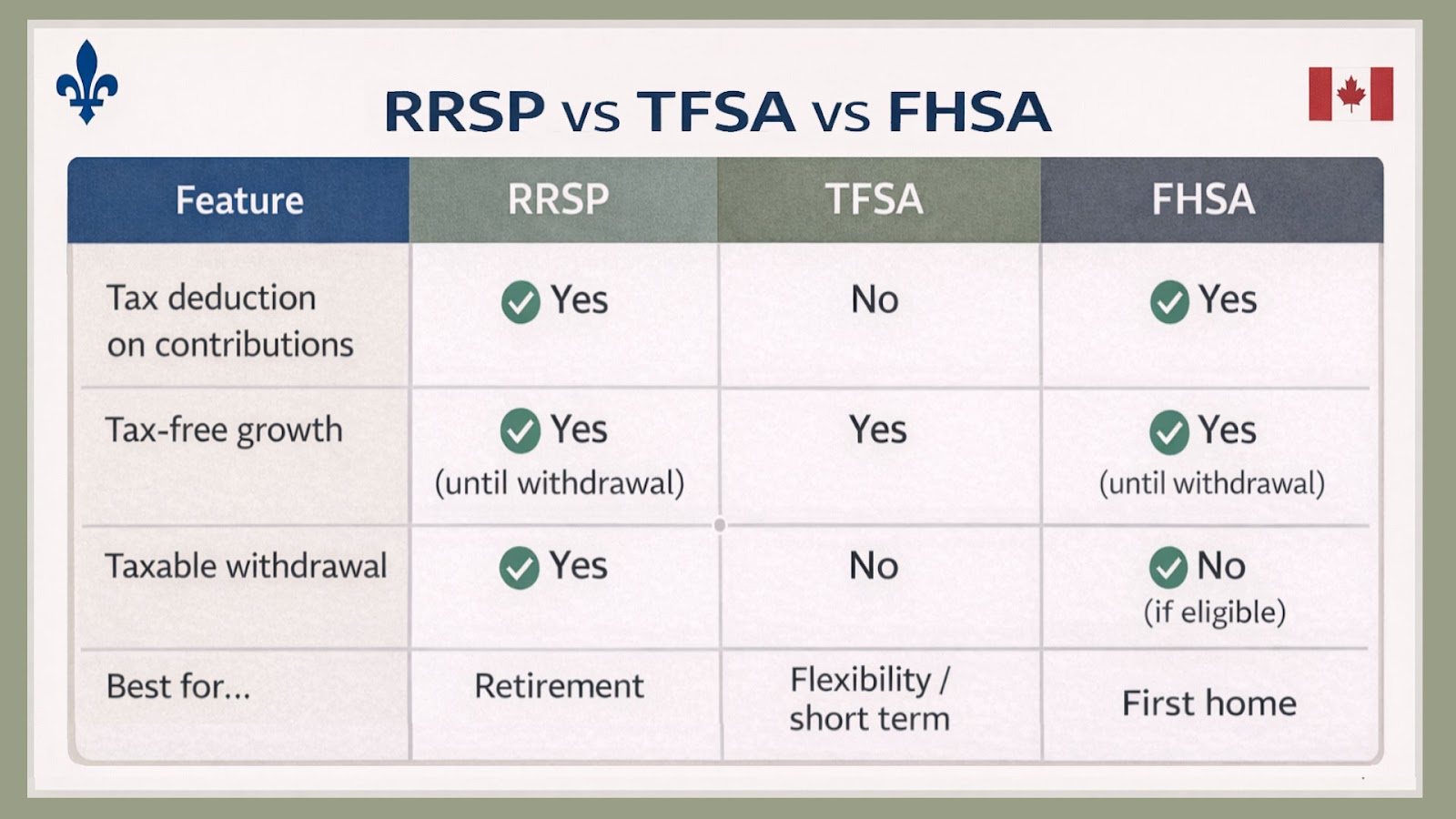

RRSP vs TFSA vs FHSA for February decisions

| Goal / Situation | RRSP in February | TFSA / FHSA Alternative |

| High income, stable job | Strong deduction now, tax-deferred growth | TFSA for flexibility, FHSA if first home eligible |

| Planning home purchase in 3–5 years | Use RRSP for HBP if disciplined | FHSA first, TFSA for shorter-term funds |

| Uncertain income next few years | Consider smaller RRSP, keep deduction unused | TFSA for emergency and mid-term goals |

| Expecting much higher income later | Contribute now, carry forward deduction | Combine RRSP + TFSA for tax flexibility |

For first‑time buyers, it is important to remember that the FHSA and the RRSP Home Buyers’ Plan can be used together. You can build FHSA savings for tax‑deductible, tax‑free withdrawals and also use HBP to access up to $60,000 from your RRSP, significantly boosting your total down payment when coordinated properly.

Strategic RRSP vs. TFSA Decisions for Quebec Residents

A classic February mistake in Quebec is defaulting to an RRSP when a TFSA or FHSA would better suit your goal. Many believe "RRSP is for tax refund, TFSA is for savings," but the key question is your marginal tax rate now versus in retirement.

If your income is low or moderate, your combined Quebec and federal marginal tax rate might be 20%–28%. In this scenario, TFSA contributions can be more attractive, especially if you expect a higher future tax rate or need liquidity. RRSPs excel when your current tax rate significantly exceeds your expected retirement rate.

The Risks of Using RRSPs for Short-Term Savings

A major February error is putting money into an RRSP that you'll need within 1–2 years (e.g., for a car, move, or business). You get a deduction today but face withholding tax and full income inclusion upon withdrawal. This often leaves you worse off than using a TFSA or a high-interest savings account.

RRSPs are ideal for long-term goals like retirement (and sometimes the Home Buyers’ Plan or Lifelong Learning Plan). If uncertain, splitting your February contribution between RRSP and TFSA offers a safe middle ground until you consult a planner.

Integrating February Contributions into Your Retirement Plan

Another major mistake is treating February RRSP deposits as separate from your overall retirement planning. Many Quebec workers contribute "whatever is left" instead of determining how much their RRSP needs to contribute to their retirement income target.

A 2026 RBC and Statistics Canada trend indicates many Canadians underestimate their lifespan and retirement costs, particularly with inflation and Quebec housing. A random RRSP contribution schedule can lead to being asset-rich but income-poor, or overly reliant on CPP/QPP and Old Age Security.

Coordinating RRSPs with Mortgage and Debt Management

Some Quebec families rush February RRSP contributions while carrying high-rate unsecured debt or facing upcoming mortgage renewals at higher interest rates. A blended approach is sometimes smarter: pay down costly debt, make a smaller RRSP deposit, then plan increased recurring contributions from each paycheque once the debt burden lessens.

A structured retirement plan reveals whether an extra $2,000 in an RRSP or an extra $2,000 paid against your mortgage principal offers greater long-term net worth. The answer depends on your interest rate, tax bracket, and timeline.

Real Quebec Case Studies: Learning from RRSP Contribution Errors

Case 1: Overcontribution and missed opportunity

A self‑employed IT consultant in Montreal received a panic email from CRA in March regarding possible RRSP overcontributions. He had relied on his bank app’s “available RRSP room,” not his Notice of Assessment.

Problem:

• He exceeded his RRSP limit by roughly $5,000.

• He also had a very uneven income and a large tax bill from the prior year.

Solution:

• We reviewed his CRA My Account, calculated the exact overcontribution, and arranged a timely withdrawal of the excess to limit the 1% per month penalty.

• We prepared a detailed RRSP and tax plan for the next 3 years, linking his corporate dividends and salary mix to his RRSP strategy.

• As part of this process, we modelled several 3‑year scenarios, showing how different RRSP contribution patterns and income mixes would affect his marginal tax rates and long‑term retirement funding.

Result:

• Penalties were minimized, and he avoided a repeat error.

• Over three years, coordinated RRSP contributions and tax planning reduced his combined Quebec and federal tax by several thousand dollars, with a consistent retirement funding plan in place.

Case 2: Wrong account choice for near‑term home purchase

A young couple, both newcomers to Quebec, made large February RRSP contributions because friends told them it was “the best tax move.” They planned to buy their first home within two years.

Problem:

- Most of their savings were locked in RRSPs, but they had not used the FHSA or fully funded their TFSAs.

- They risked either early RRSP withdrawals (and tax) or not having enough liquid funds for closing costs and moving expenses.

Solution:

- We created a 24‑month plan: stop new RRSP contributions for now, maximize FHSA for each spouse, and use TFSA for flexible savings.

- We preserved existing RRSPs for the eventual Home Buyers’ Plan, but avoided adding short‑term funds there.

Result:

- They stayed on track for their home purchase with a more tax‑efficient mix of FHSA, TFSA, and RRSP.

- Their long‑term retirement planning remained intact, and they learned how to use Quebec tax rules and federal programs together more effectively.

FAQ

1. What is the biggest February RRSP contribution mistake for Quebec residents?

Relying on the deadline instead of a plan: rushing a contribution without checking CRA RRSP room, marginal tax rate, or how it fits your retirement and debt strategy.

2. Should I always claim my February RRSP contribution on this year’s Quebec tax return?

Not always. If your 2025 income was unusually low (for example due to parental leave, studies, or a career break), it can make sense to contribute before the deadline but carry the deduction forward to a future year when you expect to be in a higher tax bracket. This way, the same RRSP dollar can produce a larger combined Quebec and federal tax saving.

3. How do I know if RRSP or TFSA is better for my February savings?

Compare your current and expected future tax brackets. If your current rate is high and retirement rate likely lower, RRSP is usually better. If your income is low/variable or you need flexibility, TFSA (and FHSA for first‑time buyers) may be more appropriate.

4. Can I fix an RRSP overcontribution made in February?

Yes, but you must act quickly. You may need to withdraw the excess and possibly file specific CRA forms to reduce the 1% per month penalty. Professional help is recommended to avoid extra tax and reporting errors.

5. How can a financial planner help with February RRSP contributions in Quebec?

A planner can align your RRSP, TFSA, FHSA, mortgage, and debt decisions; check your CRA data; optimize your Quebec tax return; and build a long‑term retirement plan so February is a confirmation step, not a panic rush.

Ready to transform your last‑minute RRSP rush into a clear, tax‑efficient strategy tailored to Quebec rules?

Book your free, no‑obligation consultation and get a personalized RRSP, TFSA, and FHSA game plan that matches your income, debts, and retirement goals.

Phone: +1-514-834-5558

Email: contact@bkfinancialservices.ca

Website: https://bkfinancialservices.ca

Consultations available in English, French, Russian, and Hebrew.

Disclaimer: This article is provided for informational purposes only and does not constitute personalized tax, legal, or financial advice. Tax rules, marginal brackets, and CRA deadlines (such as the March 2, 2026 deadline for the 2025 tax year) are subject to change. Overcontributing or making ill-timed withdrawals can result in significant tax penalties. Always consult with a qualified financial planner or tax professional to review your specific situation before making major financial decisions.