Self-employed individuals, those with rental income, investment income, or multiple paychecks often receive instalment payment requests from the CRA or Revenu Québec in the mail. Many Quebec residents mistake these notices for late tax bills or penalties, ignoring them until heavy interest accrues.

Instalment payments are simply mandatory prepayments of your current-year income tax, functioning much like the source deductions taken from a regular employee's paycheck. Understanding how they work and preparing for the upcoming June 15 payment deadline can save you significant interest charges and cash flow stress.

As a financial planner for Quebec individuals, families, and small businesses, I frequently see avoidable panic around the June 15 instalment deadline.

This guide explains CRA instalment payments, Revenu Québec instalment payments, how to seamlessly integrate them into your tax strategy and how Quebec residents can prepare for the June 15 deadline without unnecessary interest.

Understanding Tax Instalments in Quebec

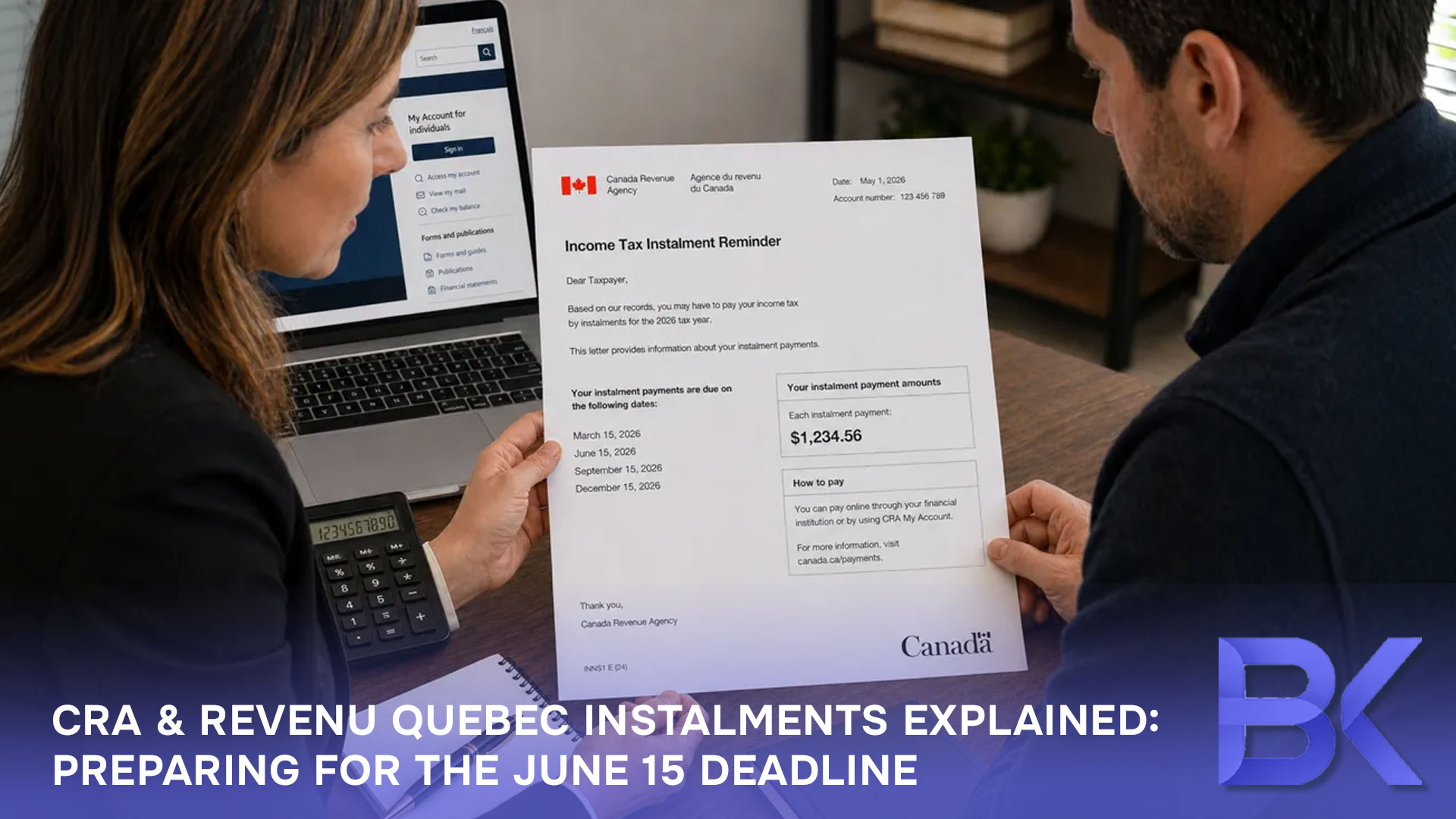

Tax instalments are prepayments of the income tax you are expected to owe for the current 2026 year. Instead of paying one massive balance on April 30 of next year, the government requires certain taxpayers to pay their tax in four quarterly instalments: March 15, June 15, September 15, and December 15.

Due to the growing gig economy, freelance work, and rising investment income, more Canadians are being required to pay instalments because tax is not automatically withheld at the source of this income. Importantly, Quebec residents face a dual system: you may have obligations to both the CRA (for federal taxes) and Revenu Québec (for provincial taxes).

If your net tax owing is high enough to require instalments, the CRA or Revenu Québec will send you reminders. For federal instalments, Quebec residents are generally subject to the $1,800 threshold, while residents of other provinces are generally subject to the $3,000 threshold.

If you receive an instalment reminder, review it carefully. When instalments are required, missing or underpaying them can lead to interest charges, even if you later pay your full balance by the regular filing deadline.

CRA and Revenu Québec Instalment Thresholds

The rules for Quebec residents are unique. You are generally required to pay tax by instalments if your net tax owing exceeds $1,800 for the current year and for either of the two previous years.

- Federal (CRA): You must pay CRA instalments if your net federal tax owing is over $1,800.

- Provincial (Revenu Québec): You must pay provincial instalments if your net Quebec tax owing is over $1,800.

For instance, if you owed $3,500 at tax time in 2024 or 2025, and you expect a similar tax bill for 2026, you will be placed on the instalment radar for both agencies. Newcomers, self-employed professionals, and investors with dividend or rental income are especially prone to crossing this $1,800 limit.

Advance planning with your financial advisor can help estimate your current-year tax and identify strategies to legally reduce your overall tax bill.

Instalment Calculation Options

The CRA provides three methods for calculating instalments (and Revenu Québec follows a similar structure):

- The No-Calculation Method: You simply pay the exact amount requested on the reminders they mail you. This is the safest option to avoid interest.

- The Prior-Year Method: You calculate your payments based entirely on last year's tax owing.

- The Current-Year Method: You estimate your actual income for 2026 and pay based on that projection.

If your income is dropping significantly this year (e.g., entering retirement, taking maternity leave, or after selling a highly profitable property last year), the current-year method can save your cash flow. However, it carries a risk: if you underestimate your income and underpay your instalments, the CRA and Revenu Québec will penalize you with interest.

The June 15 Instalment "Double Deadline"

The June 15 instalment date is critical. For many self-employed Quebec residents, June 15 is a “double deadline” because it is both the due date for the second instalment and the filing deadline for individuals with self-employment income. This filing deadline applies to self-employed individuals and their spouses/common-law partners who are required to file on that later date.

Missing or underpaying the June 15 instalment results in compound interest charged from that exact date until the payment is made. Catching up in September does not erase the interest accrued over the summer. For commission workers or consultants, building a monthly tax reserve ensures the June 15 payment does not cause a cash crisis.

How to Prepare for the June 15 Payment

Preparation begins with a realistic projection of your 2026 annual income. If your income will be similar to 2025, simply paying the amount on the CRA and Revenu Québec reminders is your safest bet.

Next, integrate this payment into your budget. Treat it like a recurring utility bill: divide the required quarterly amount by three, and set aside that money into a separate "tax savings" account each month. This transforms lump-sum panic into predictable spring cash flow planning.

If the June payment feels tight, set aside the amount monthly between now and then so the instalment does not disrupt your operating cash flow.

Payment Timing Strategies for CRA Instalment Payments

| Strategy | How It Works | Best For |

| Pay on Due Dates Only | Pay full amounts on Mar 15, Jun 15, Sept 15, Dec 15 | Stable income, strong cash reserves |

| Monthly Tax Savings Account | Set aside 1/12 of estimated annual tax each month | Self-employed, variable income |

| Accelerated Pre-funding | Overpay early instalments to reduce later ones | High early-year income, commission earners |

Quebec Tax Planning: Managing Both Agencies

Quebec residents must manage both federal CRA instalments and Revenu Québec instalments. Each authority issues its own notices and requires separate payments.

Professionals, small incorporated business owners, and rental property investors in Quebec benefit greatly from an integrated plan. A financial planner can align your federal and provincial instalments with available deductions – such as RRSP contributions, pension income splitting, and business expenses – ensuring you never overpay while remaining strictly compliant.

Using RRSP Contributions to Manage Instalment Needs

RRSP contributions significantly reduce your net tax owing, which can lower or even eliminate your need to pay instalments. RRSP deductions can be especially useful if you are expecting bonus income, rental income, or a profitable business year and want to reduce your current-year balance owing.

Timing is key: RRSP contributions made during 2026 can reduce your 2026 net tax owing if you deduct them on your 2026 return, which may lower later instalments under the current-year method.

For clients nearing retirement, this strategy must be balanced. Over-contributing to an RRSP just to avoid a $2,000 instalment today might inadvertently increase your taxable income during retirement, potentially triggering Old Age Security (OAS) clawbacks.

A financial planner can model contribution levels and timing to illustrate effects on instalment requirements, April 30 balances, and retirement income. This data-driven approach is useful as more Canadians work past 65 with mixed income sources.

Cash Flow Planning for Instalments

The primary challenge with tax instalment payments is rarely the tax itself—it is the shock of fitting four massive lump-sum payments into an everyday budget. Strategic cash flow planning transforms these stressful payments into predictable, manageable items.

Start by listing all your fixed monthly commitments (mortgage, utilities, debt payments) and then layer on your annual or quarterly expenses (property tax, insurance, and CRA/Revenu Québec instalments). This macro-overview immediately reveals which months will have tight cash flow, highlighting exactly where you need to adjust your spending in advance.

If you are carrying high-interest consumer debt, managing instalments becomes a balancing act. A financial planner can help you prioritize aggressive debt reduction while still meeting your strict government instalment requirements. Often, this involves temporarily pausing voluntary investments or adjusting your savings rate until the high-interest debt is cleared and your tax obligations are stabilized.

Setting Up Automatic Payments

Pre-authorized debit payments can be set up via your bank, CRA My Account, and Revenu Québec's My Account for Individuals. If your income is changing materially, review your instalment estimate before the next due date rather than waiting until year-end. Automating payments guarantees you will never miss the June 15 deadline due to simple oversight.

However, automation should not replace a mid-year review. If your business income drops sharply in the summer, you should review your instalment plan with an advisor before September to ensure you aren't sending the government money you actually need for your business.

For Quebec residents with complex finances, aligning CRA automatic payments with Revenu Québec arrangements and other financial commitments aids overall stability. A coordinated calendar with a planner can be highly effective.

Real Quebec Cases: Instalments in Practice

Case 1: Self-Employed Consultant Facing a June Cash Crunch

A Montreal IT consultant had strong business income but zero tax withheld at source. After her tax balances crossed the $1,800 threshold, both the CRA and Revenu Québec requested instalments. Assuming they were optional, she ignored the notices and was shocked to receive heavy interest penalties, even though she paid her full tax balance on time in April. We projected her 2026 income and advised automatically moving 28% of her monthly invoices into a dedicated tax account. When June 15 arrived, the funds were already there. She avoided all interest charges and completely eliminated the stress of next year's tax season.

Case 2: Retired Couple with Surging Investment Income

A Laval couple had CPP/QPP, OAS, pensions, and a growing non-registered stock portfolio. The taxes on their dividend income pushed them over the instalment threshold. The couple worried the June 15 payment would interfere with their plan to help their child buy a first home. We developed a multi-year plan that included strategic TFSA withdrawals instead of taxable account withdrawals. By safely recalculating their 2026 income using the current-year method, we reduced their required instalments by 25%. This freed up cash flow for their child's down payment without increasing their long-term tax burden.

FAQ

1. What are tax instalment payments and why did I receive a reminder?

Instalment payments are mandatory quarterly prepayments of your income tax. You receive a reminder when your net tax owing exceeded $1,800 for the CRA or Revenu Québec in the previous years, meaning the government expects you will owe tax again this year.

2. Is the June 15 instalment payment mandatory?

Yes. If you receive an instalment reminder and your financial situation hasn't drastically changed, payment by June 15 is legally required. The CRA and Revenu Québec will charge you compound interest for late or underpaid instalments.

3. How can I reduce or avoid instalment payments in the future?

You can lower your net tax owing by increasing your RRSP contributions, requesting that more tax be withheld at source from your pension or salary, and diligently claiming all eligible business expenses.

4. What if my income dropped and the instalment amounts seem too high?

You can use the "Current-Year Method," which allows you to estimate your actual 2026 tax and pay a lower instalment amount based on that calculation. However, if you estimate incorrectly and underpay, you will be hit with interest charges. Always seek professional help to run a precise projection first.

5. How do CRA instalment payments interact with Revenu Québec instalments?

They operate independently. Because the threshold for both is $1,800, you may owe instalments to one, both, or neither. You must make separate payments to the CRA and Revenu Québec to satisfy both obligations.

Stop Stressing Over Your June 15 Tax Payments

Whether you are newly self-employed, a retiree with investment income, or a freelancer, you don't have to navigate CRA and Revenu Québec instalments alone. A proactive cash flow and tax plan ensures your June 15 payment fits smoothly into your budget without triggering penalties or depleting your savings.

Book Your Free Consultation Today:

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

Consultations available in English, French, Russian, and Hebrew.

Let's optimize your tax strategy for 2026!

Disclaimer: This article is provided for general informational purposes only and does not constitute personalized financial, tax, or legal advice. Tax laws, instalment thresholds ($1,800 for Quebec residents), and CRA/Revenu Québec procedures are subject to change. Always consult with a qualified financial planner or tax professional to evaluate your specific situation and ensure compliance with tax authorities before adjusting your instalment payments.