When your Notice of Assessment (NOA) from Revenu Québec and the Canada Revenue Agency (CRA) arrives in the mail or your online portal, resist the urge to just file it away.

Your Notice of Assessment is more than a tax receipt – it's your annual checkpoint confirming your entire tax profile, RRSP limits, benefits eligibility, and future planning opportunities. Costly mistakes, miscalculations, and missed refunds often hide within these documents.

This official notice confirms your tax return: what was accepted, what was changed, and your final tax balance or refund. A careful review protects you from accumulating interest, unexpected penalties, and lost government benefits.

Whether you filed early and just received your notice, or are preparing for its arrival, here are 10 critical checks explained simply for Quebec taxpayers – including employees, self‑employed individuals, newcomers, and small business owners.

How to Read Your Quebec Notice of Assessment: Key Checks

Quebec taxpayers receive two separate Notices of Assessment in Quebec: one provincial (Revenu Québec) and one federal (CRA). Both require careful review, as errors in either can impact your total tax bill and future financial plans.

Combined federal-Quebec marginal tax rates can exceed 53% for high earners. Even middle‑income households can see hundreds of dollars in differences due to minor adjustments in income, RRSP deductions, or credits.

Verify these first three items as soon as you open your notice:

1. Personal Information and Marital Status Accuracy

Confirm your name, address, social insurance number, and marital status. An incorrect marital status affects your eligibility for refundable tax credits, the solidarity tax credit, the GST/HST credit, and family benefits.

If your marital status changed, ensure it’s updated on both federal and Quebec files. Errors here can lead to immediately lost monthly benefits.

2. Review Taxable and Net Income Figures

Compare the “taxable income” and “net income” on your NOA to the tax return you filed. This is crucial if you have multiple T-slips or RL-slips, self‑employed income, or foreign income.

CRA and Revenu Québec match slips already filed by your employers/banks, which may increase your assessed income if you missed reporting them. This can reduce benefits tied to net income and affect student loan repayments.

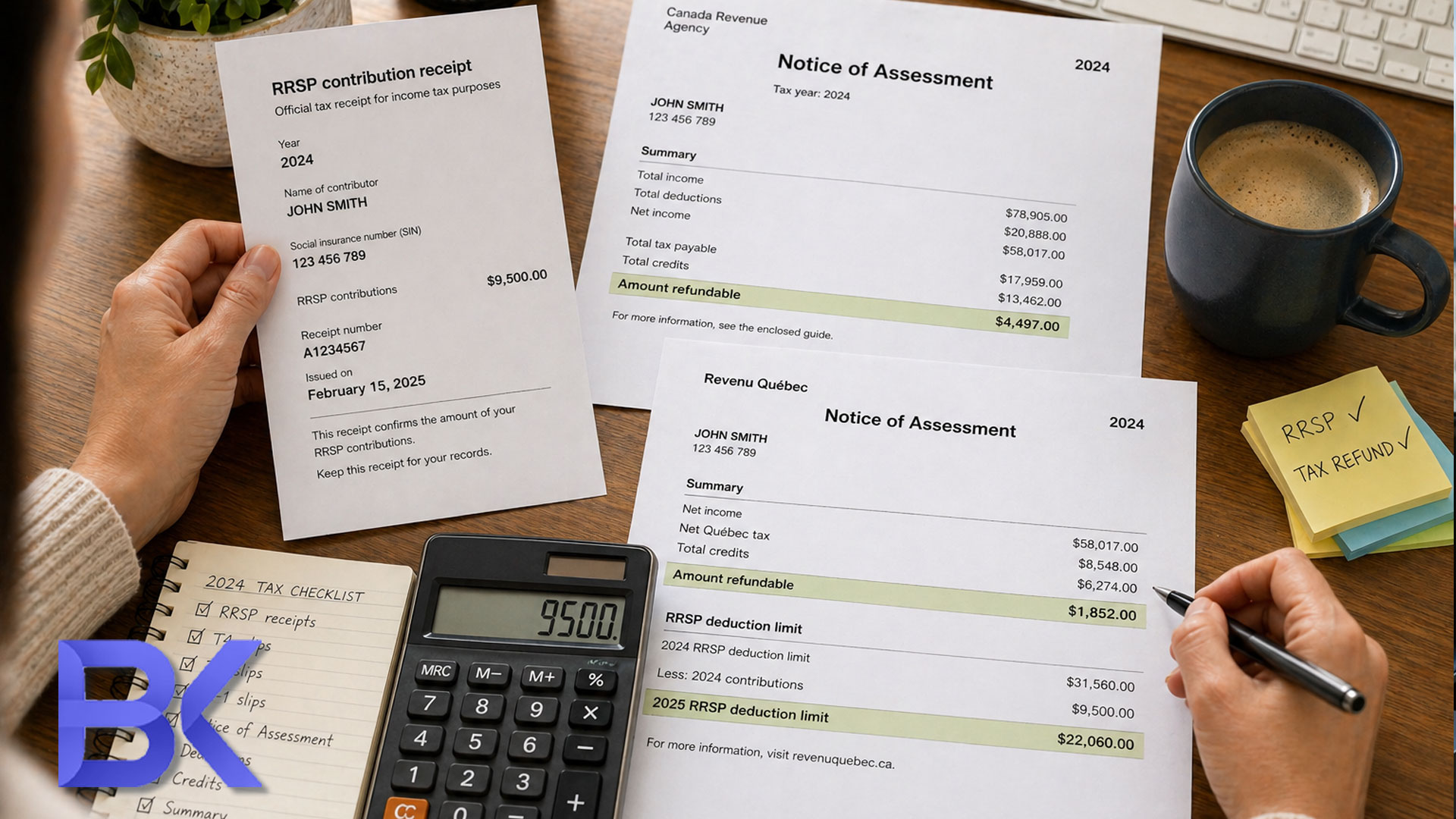

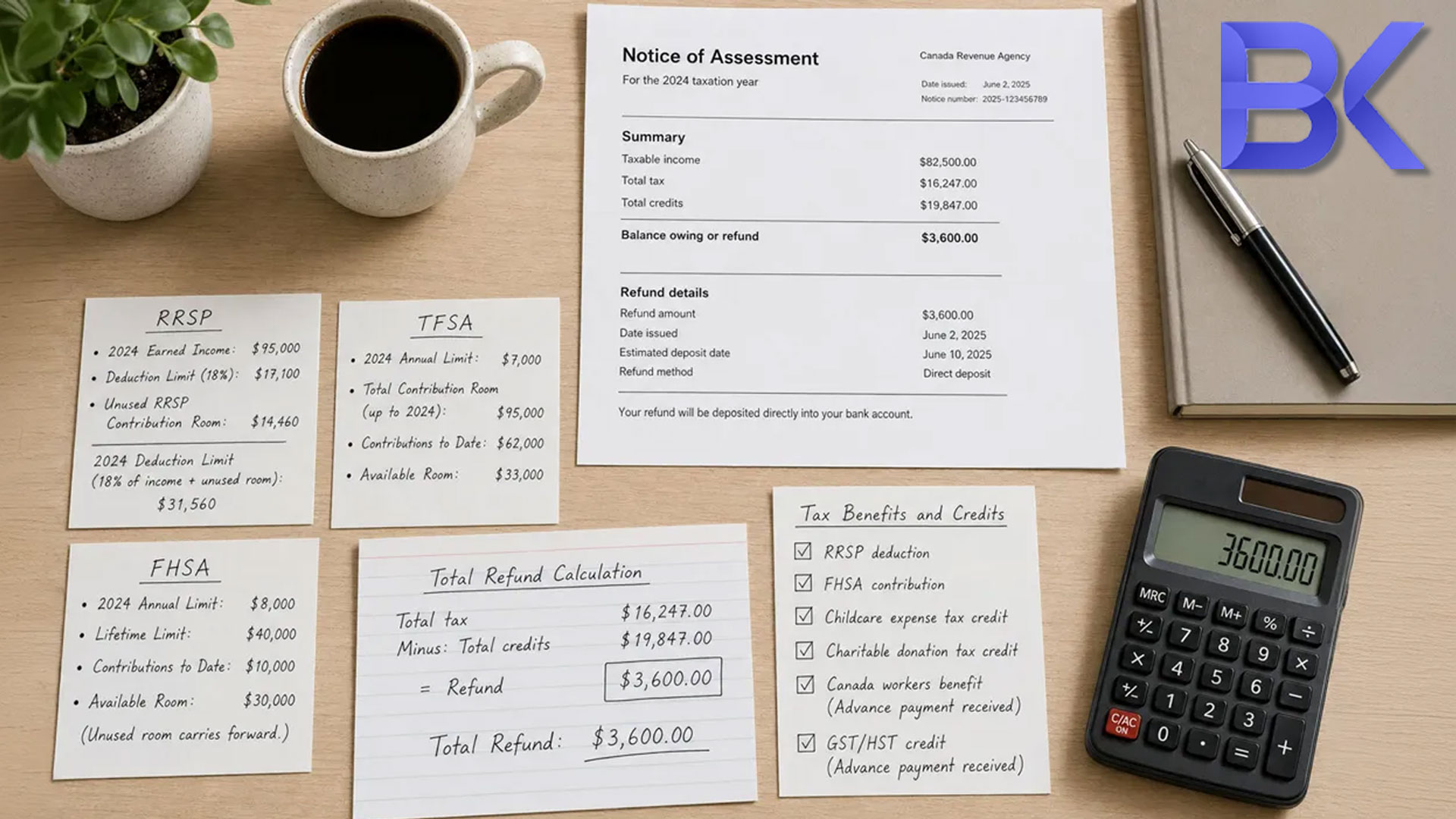

3. Verify RRSP Contributions and 2026 Deduction Limits

Check that your reported RRSP contributions match your receipts. The federal NOA shows your "RRSP deduction limit for 2026" – the maximum you can contribute and deduct for 2026 (not for your 2025 return).

Discrepancies between agency data and your financial provider can lead to under‑deducting (overpaying tax) or over‑deducting (risking a 1% per month penalty). Professionals and self‑employed individuals often use RRSP room strategically.

Impact of Tax Deductions on Your Notice of Assessment

Deductions lower your taxable income; credits directly reduce your tax payable. When the CRA or Revenu Québec adjusts these during their automated review, your refund amount may change unexpectedly.

Missing a significant deduction or credit can easily cost you $500-$2,000. Focus on these key areas.

4. Employment Expenses and Self-Employment Deductions

Review any adjustments made to claimed employment expenses (home office, vehicle, tools) or self‑employed business expenses. The agencies might disallow certain items or request documentation later.

Early detection allows you time to appeal or gather necessary receipts and logbooks before a formal audit begins. This is especially relevant for those working remotely or with side businesses.

5. Tuition, Education, and Credit Transfers

Students and parents in Quebec use tuition and education credits, which can be transferred. Verify:

- Total eligible tuition claimed

- Amount carried forward to future years

- Amount transferred to or from a spouse or parent

Errors can delay future credit claims or reduce transfer amounts within families.

Summary: What to Look For and How to React

| Aspect | Writing Evaluation | Speaking Evaluation |

| Task focus | Format, structure, register | Interaction, spontaneity, adaptation |

| Planning time | Longer, you can draft and revise | Short prep, performance is live |

| Error tolerance | Slightly stricter on grammar and spelling | More tolerant if communication is clear |

| Key success factor | Organized, complete response | Fluency and ability to keep communication flowing |

Priority Checks: What to Do First vs Later

IMMEDIATE (Today – 30 minutes):

- Personal information & marital status [web:95]

- Taxable income vs filed return

- RRSP deduction limit for next year

LATER REVIEW (This Week):

- Employment/business expenses

- Carryforward amounts

- Credits and instalment history

PROFESSIONAL FOLLOW-UP (Book Now):

- Large balance owing/interest

- Significant agency adjustments

- Complex pension adjustments or multiple NOAs

Retirement and Financial Planning Insights

Your Notice of Assessment is not just a tax receipt; it is a crucial financial planning document. RRSP limits, pension adjustments, and income figures guide your future savings strategy.

A quick review can reveal simple ways to improve long-term retirement outcomes and optimize current cash flow, even amidst financial pressures.

6. RRSP Room, Pension Adjustment, and Employer Plans

Your NOA shows the pension adjustment from employer plans, which reduces your RRSP room available NEXT YEAR (2027 if reviewing 2026 NOA). Examine these items beyond your RRSP deduction:

- Pension adjustment (for group RRSPs or pension plans)

- Past service pension adjustment, if applicable

- New RRSP room created this year

Employer pension plan adjustments directly reduce your new RRSP room. Coordinating your personal RRSPs with employer plans prevents accidental over-contributions.

7. FHSA, TFSA, and Other Registered Accounts

The Notice of Assessment connects to your broader savings strategy, including the First Home Savings Account (FHSA) and Tax‑Free Savings Account (TFSA). Your assessment figures dictate your available room for tax-advantaged accounts.

For Quebec first-time buyers, combining RRSP Home Buyers’ Plan withdrawals with FHSA contributions is effective. Knowing your exact income and deduction limits helps determine the optimal allocation between an RRSP (for the Home Buyers' Plan), an FHSA, and a TFSA for tax efficiency and flexibility.

8. Review Credits, Benefits, and Overpayments

Check the listed tax credits and benefits:

- Solidarity tax credit (Quebec)

- GST/HST credit

- Canada Child Benefit and Quebec child assistance amounts (indirectly linked)

Many credits (solidarity tax credit, GST/HST, family allowances) are income-tested and vary by Quebec family size and situation.

Understand the reasons for any overpayments or clawbacks shown. These may stem from income changes, marital status updates, or missed notifications. Addressing this now prevents unexpected debt collections next year.

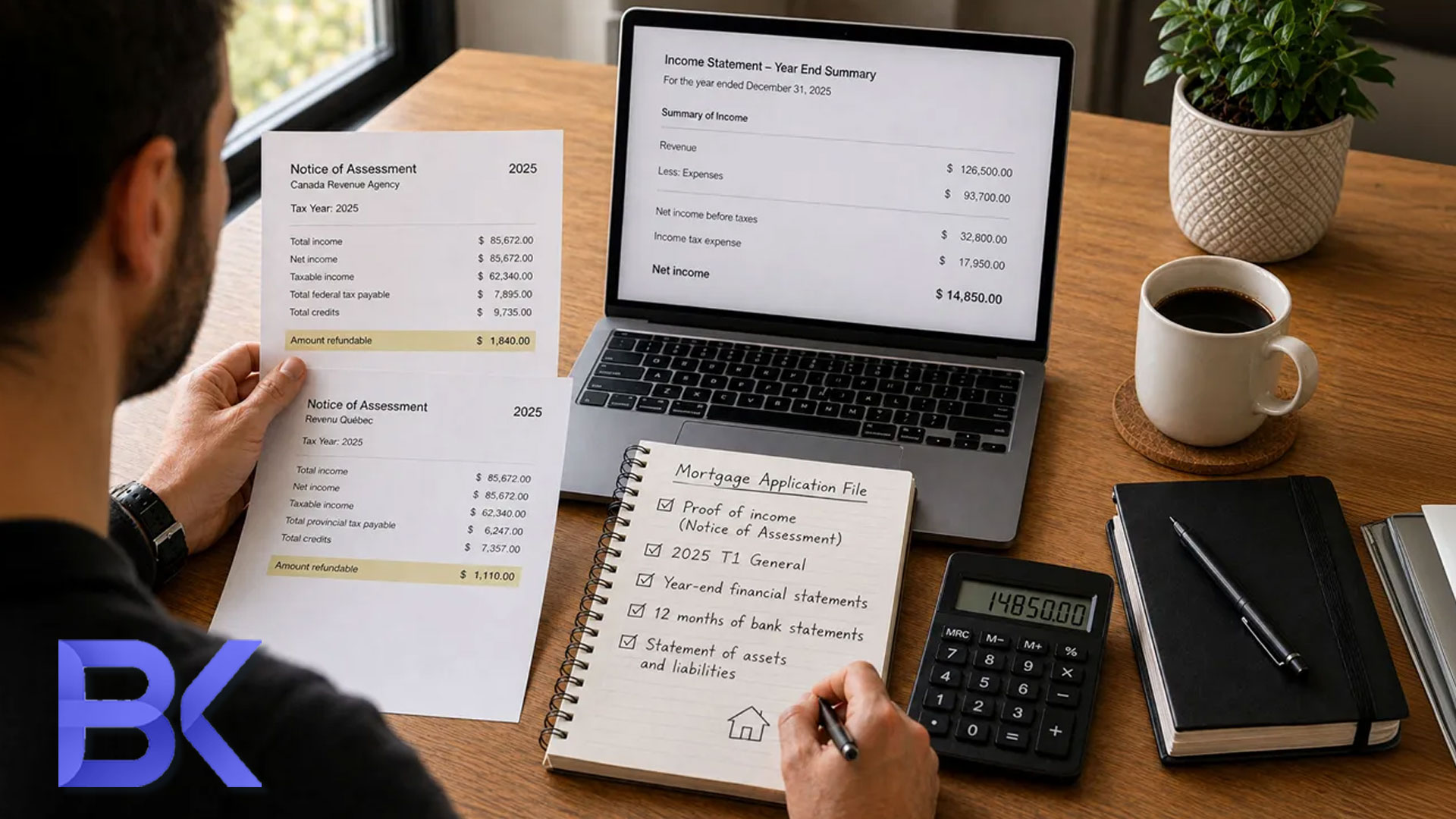

Mortgages and Cash Flow Considerations

Lenders often require recent Notices of Assessment for mortgage applications or renewals, particularly for Quebec self‑employed individuals. An accurate assessment simplifies this process and can improve approval chances.

Your tax situation directly affects monthly cash flow, impacting your ability to manage mortgage or rent payments comfortably.

9. Check Balance Owing, Interest, and Payment Deadlines

If you owe tax, verify:

- The precise balance due (federal and Quebec)

- Any applied interest or penalties

- Payment due dates and available options

Late payments in Quebec incur daily interest that accumulates quickly. If cash flow is tight, arrange a payment plan or adjust instalments instead of ignoring the debt.

10. Carryforward Amounts: Losses, Credits, and Instalments

Review amounts eligible for carryforward:

- Non‑capital and capital losses

- Unused tuition or education credits

- Unused RRSP contributions

- Paid instalments that may reduce future balances

These carryforward amounts are valuable for future tax planning, debt reduction, and investment strategies. Maintaining records and annual reviews aids strategic use.

2 Real Cases

Case 1 – Missed RRSP deduction and $1,800 refund recovered

A Montreal engineer received a smaller‑than‑expected refund on his Quebec and federal Notices of Assessment. A late RRSP contribution wasn't reported in time by the financial institution. His assessment showed higher RRSP room, indicating a missing slip.

After obtaining the slip and filing an adjustment with Revenu Québec and the CRA, he received an additional $1,800 refund. His RRSP room was updated for the following year, allowing for a more efficient contribution plan.

Case 2 – Self‑employed expenses and mortgage approval

A self‑employed IT consultant in Laval was denied a mortgage due to low reported net income and inconsistent figures on her NOA compared to her bookkeeping.

Reviewing her past assessments revealed misclassified business expenses and unclaimed legitimate costs. After restructuring her bookkeeping and filing adjustments for two years, her true net income was clarified. She obtained mortgage approval using the corrected Notices of Assessment.

FAQ

1. What is the most important thing to check on my Notice of Assessment?

Prioritize your personal information, taxable income, net income, and RRSP deduction limit. Inaccuracies here affect your Quebec taxes, monthly benefits, and ability to save for retirement next year.

2. How does my Notice of Assessment affect retirement planning in Quebec?

It officially confirms your RRSP deduction limit and pension adjustment, showing exactly how much you can contribute to your RRSP in 2026 without overcontribution penalties. TFSA and FHSA limits are tracked separately.

3. Can I change my return after reviewing my Notice of Assessment?

Yes. If you find errors or missed deductions (like a late T-slip), you can request an adjustment (T1-ADJ for CRA, TP-1.R for Revenu Québec). Supporting documents are typically required.

4. Do lenders look at my Notice of Assessment for mortgages in Quebec?

Yes. Lenders use your two most recent Notices of Assessment to verify your income, confirm tax compliance, and ensure you have no outstanding tax debts before approving a mortgage.

5. When should I call a financial planner about my Notice of Assessment?

Consult a planner immediately if you see unexpected changes made by the government, large balances owing, or if you need help integrating your newly confirmed RRSP room into a long-term investment strategy. This is best done before the next tax season.

Don't Let Errors on Your Notice of Assessment Cost You Money

A 30-45 minute review of your Notice of Assessment can identify missed refunds, clarify your tax position, and integrate your taxes with your retirement, mortgage, and investment planning.

Book a Free Consultation Today:

Phone: +1-514-834-5558

Email: contact@bkfinancialservices.ca

Site: https://bkfinancialservices.ca

Consultations available in English, French, Russian, and Hebrew. Reach out to secure your financial plan for 2026!

Disclaimer: This article is provided for general informational purposes only and does not constitute personalized financial, tax, or legal advice. Information regarding Notices of Assessment, tax brackets, and CRA/Revenu Québec procedures is subject to change. Always consult with a qualified financial planner or tax professional to evaluate your specific Notice of Assessment and financial situation.