Tax season often prompts a deep financial review. If you find yourself with a tax refund or surplus spring cash, it raises one of the most common personal finance questions: should I pay down debt or invest?

For many Quebec taxpayers, the best after tax season decision is not simply debt versus investing, but which account or loan gives the strongest after-tax result.

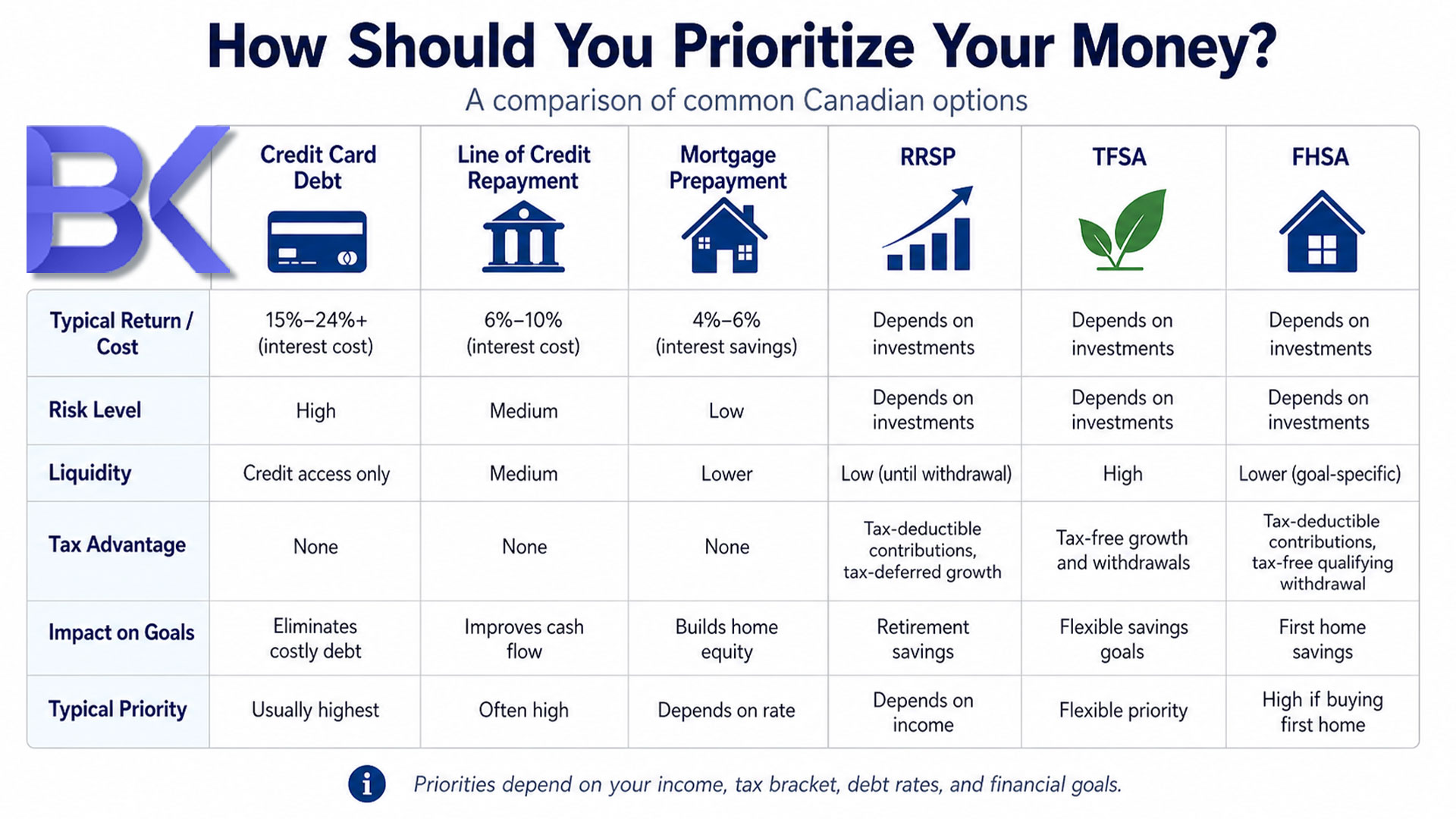

In the current interest rate environment, deciding between paying down credit cards, lines of credit (LOCs), or mortgages versus investing in RRSPs, TFSAs, or FHSAs is critical. The wrong choice can cost you significantly in interest and lost growth.

As a financial planner, I guide Quebec residents, newcomers, and professionals through a practical, numbers-first approach to allocating extra dollars after tax season.

Tackling High-Interest Credit Card Debt

Credit card balances should usually be your first priority when deciding your financial next steps. In 2026, credit card interest rates in Canada often range around 19–24% annually, with some retail cards charging even more. For most households, it is difficult for a conservative investment to reliably outperform that after fees and taxes.

Paying off high-interest credit card debt is often comparable to earning a tax-free return equal to the interest rate you no longer have to pay. For almost all households, aggressively tackling credit cards before investing (beyond securing an employer pension match) is the most efficient wealth-building strategy.

How to prioritize multiple credit cards

List your credit cards by interest rate, not balance. Focus on the card with the highest rate first (the debt avalanche method), while making minimum payments on the others. Redirect all surplus cash to that top-rate card until it's cleared, then move to the next.

Once paid, move to the next highest-rate card. This approach minimizes total interest paid and frees up cash flow sooner for investments.

When it might make sense to invest instead of paying extra on credit cards

Exceptions are rare, but investing first might be logical if:

- You have a small card balance on a promotional 0–5% rate.

- You are leaving "free money" on the table by not maximizing an employer RRSP match.

- You make a well-timed RRSP contribution in a high Quebec tax bracket to generate a large tax refund, which you then use to wipe out the credit card within months.

These scenarios require a precise, time-bound plan. For most, clearing standard high-interest credit cards remains the top priority after tax season.

Managing Lines of Credit (LOCs) and HELOCs

Lines of credit, especially Home Equity Lines of Credit (HELOCs), often have lower rates than credit cards but can become long-term traps due to their flexibility. Unsecured LOCs often fall around 9–13% in 2026, while HELOC rates usually track prime plus a small margin.

This rate range places LOCs in a critical decision zone. Sometimes, aggressive repayment is best; other times, you can invest while paying them down gradually.

When to aggressively pay down your line of credit

Prioritize debt repayment if your LOC rate exceeds 8–10%, or if you are only making interest-only payments. Every extra dollar paid on a high-rate LOC offers a risk-free return equal to the interest rate. Beating a guaranteed 10% after-tax return in the stock market is incredibly difficult.

When a balanced “pay debt and invest” strategy works:

If your LOC rate is moderate (e.g., 7–8%) and your cash flow is stable, a blended strategy may suit you. You can allocate a portion of your refund to LOC repayment, and another portion to long-term investing. This works best if you have a long investment horizon (10+ years) and the discipline to not re-borrow the funds you just paid off.

A detailed paycheque analysis can determine the optimal allocation.

Comparing Debt Types and Priorities

| Type of Obligation | Typical 2026 Interest Rate | Priority After Tax Season* |

| Credit cards | 19–24%+ | Highest Priority (Clear before investing) |

| Unsecured LOC | 9–13% | High Priority (Often beats investing) |

| HELOC | Prime + 0.5–2% | Medium Priority (May blend with investing) |

| Fixed-rate mortgage | 4–7% | Lower Priority (Long-term investing often wins) |

*Assuming normal risk tolerance and no extreme situations.

Mortgage Prepayments vs. Long-Term Investing

Canadian mortgages generally have lower interest rates than unsecured debt and are tied to your home. This impacts the pay debt or invest after tax season calculation.

With 5-year fixed mortgage rates between 4–7% in 2026, prepaying your mortgage provides a guaranteed interest savings equal to your mortgage rate, subject to your mortgage terms. However, a diversified, long-term investment portfolio inside a registered account like RRSP or TFSA often yields higher expected returns over a 15 to 25-year period.

When it’s smart to pay extra on your mortgage

Consider prioritizing mortgage prepayments when:

- All credit card and high-rate LOC debt is eliminated.

- You prefer guaranteed savings over investment risk.

- You anticipate higher renewal rates and wish to reduce the balance.

- You aim to be mortgage-free before retirement.

Many Quebec mortgage contracts allow annual prepayments, often in the 10–20% of original principal range, as well as increased regular payments, but the exact terms depend on your lender and mortgage agreement. Using a tax refund for a lump-sum prepayment can significantly reduce interest costs and shorten amortization.

When investing beats extra mortgage payments

Investing may be more beneficial than extra mortgage payments if:

- Your FHSA or TFSA contribution room is not fully utilized.

- RRSP contributions generate substantial Quebec and federal tax refunds.

- Your investment horizon is 15+ years, allowing time to navigate market volatility.

A blended approach often suits young professionals and families:

1. Clear all non-mortgage, high-interest debt.

2. Contribute strategically to RRSP/TFSA/FHSA.

3. Use a small portion of your annual tax refund for a lump-sum mortgage prepayment to shorten your amortization.

Deciding Between RRSP, TFSA, and FHSA

Once costly debts are managed, the next step is deciding where to invest after tax season: RRSP, FHSA, or TFSA. Each offers distinct tax benefits influencing the pay debt or invest decision.

The FHSA is particularly advantageous for first-time homebuyers in Quebec, merging RRSP tax-deductible contributions with TFSA tax-free withdrawals for a qualifying home purchase. Properly utilized, it can accelerate down payment savings while providing immediate tax relief.

When RRSP contributions make sense before extra debt payments

RRSP contributions can still be attractive even with some medium-rate debt remaining, particularly if the refund is used quickly to reduce debt or if your employer offers an RRSP match.

Employer RRSP matching is a separate exception: if your workplace match is available, it usually deserves priority before extra voluntary debt repayment.

This “RRSP – refund – debt” strategy can outperform direct debt repayment for certain income levels. The optimal choice depends on your marginal tax rate, interest rate, and time horizon, often requiring detailed financial analysis.

Why TFSA flexibility matters if you still have some debt

A TFSA offers tax-free growth and withdrawals without an upfront tax deduction. If your current income is low or you need financial flexibility (e.g., self-employed, variable income, newcomer to Quebec), starting with a TFSA can be a safer approach.

Should an emergency arise, TFSA withdrawals are tax-free and flexible, with contribution room restored in the following calendar year, which can help you avoid high-interest credit. This makes the TFSA a valuable tool for maintaining financial stability once expensive debt is eliminated.

For a broader spring budgeting framework, see our guide on spring cash flow after RRSP, which shows how to coordinate refunds, debt payments, childcare, and savings goals.

Real Client Scenarios

Case 1 – Young professional with credit cards and a LOC

A Montreal software engineer received a $2,800 tax refund. He had $9,000 in credit card debt at 19.99% and a $15,000 line of credit at 10.5%. He wanted to start a TFSA.

The Plan: We delayed the TFSA. He applied the entire $2,800 refund to the 19.99% credit card and restructured his monthly cash flow to clear the rest of the cards within 12 months.

Result: By avoiding the high-interest credit card balance, his net worth improved much faster than if he had invested that money while carrying the debt.

Case 2 – Couple deciding between mortgage prepayment and investing

A Laval couple in their mid-30s held a $360,000 mortgage at 5.2%. They had no credit card debt and received a combined $6,500 tax refund. They sought guidance on making a lump-sum mortgage prepayment versus investing for the future.

The Plan: A blended approach. They invested $4,000 into their TFSAs for long-term, tax-free growth. The remaining $2,500 was used as a lump-sum mortgage prepayment, immediately reducing their principal and saving thousands in lifetime interest.

FAQ

1. Should I always pay debt before I invest after tax season in Canada?

Not always, but high-interest credit card debt should usually be cleared first. Balancing LOCs, mortgages, and investing depends on comparing your specific interest rates against your expected investment returns.

2. Is it better to pay my line of credit or put money in my RRSP?

If your LOC rate is high (10–13%), repayment is mathematically safer. However, for Quebec taxpayers in higher brackets, contributing to an RRSP to generate a large tax refund, and then using that refund to pay the LOC, can be highly efficient.

3. Should I use my FHSA before paying extra on my mortgage?

For first-time homebuyers, the FHSA generally takes precedence over extra mortgage prepayments due to its combination of tax deductions and tax-free growth. Once FHSA room is utilized and high-interest debt is cleared, mortgage prepayments become a more compelling option.

4. If I get a tax refund, should I put it on my mortgage or in my TFSA?

If you have a low-rate fixed mortgage and a long time horizon, investing in a TFSA usually yields a higher net return over 15+ years. If you value guaranteed interest savings and peace of mind, prepaying the mortgage is a fantastic, risk-free choice.

5. How can a financial planner help decide whether to pay debt or invest after tax season?

A planner can analyze your Quebec taxes, interest rates, cash flow, and financial goals. They can model various scenarios-RRSP, TFSA, FHSA, or debt repayment-to determine the optimal mix for accelerating net worth growth within your comfortable risk tolerance.

Not sure how to allocate your tax refund or surplus cash this spring?

A financial planner can analyze your Quebec taxes, interest rates, and cash flow to determine the optimal mix for accelerating your net worth.

Book Your Free Consultation Today:

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

(Available in English, French, and Hebrew)

Disclaimer: This article is provided for general informational purposes only and does not constitute personalized financial, tax, or legal advice. Interest rates, tax brackets, and investment returns fluctuate. Always consult with a qualified financial planner or tax professional before making major decisions regarding debt repayment or investments.