In Quebec, it is incredibly tempting to direct every spare dollar you have toward paying down your mortgage, wiping out credit cards, or maximizing your RRSP, FHSA, and TFSA. The urge to build wealth or eliminate debt quickly is strong.

However, skipping step one – building a reliable emergency fund – is one of the most costly mistakes for household finances. Without a cash cushion, a sudden job loss, a medical emergency, or an unexpected home repair will instantly force you back into high-interest debt.

A solid cash reserve protects your monthly budget, prevents you from making rushed withdrawals from your registered investments, and supports much better long-term financial decisions. Here is exactly how much liquid cash Quebec households must keep on hand before accelerating debt payments or investing.

Why Quebecers Need a Strong Cash Cushion in 2026

Living costs, housing prices, and borrowing rates in Quebec remain stubbornly high in 2026. This economic reality severely elevates the importance of an emergency fund, especially for families managing rent, childcare, insurance, and summer spending pressures.

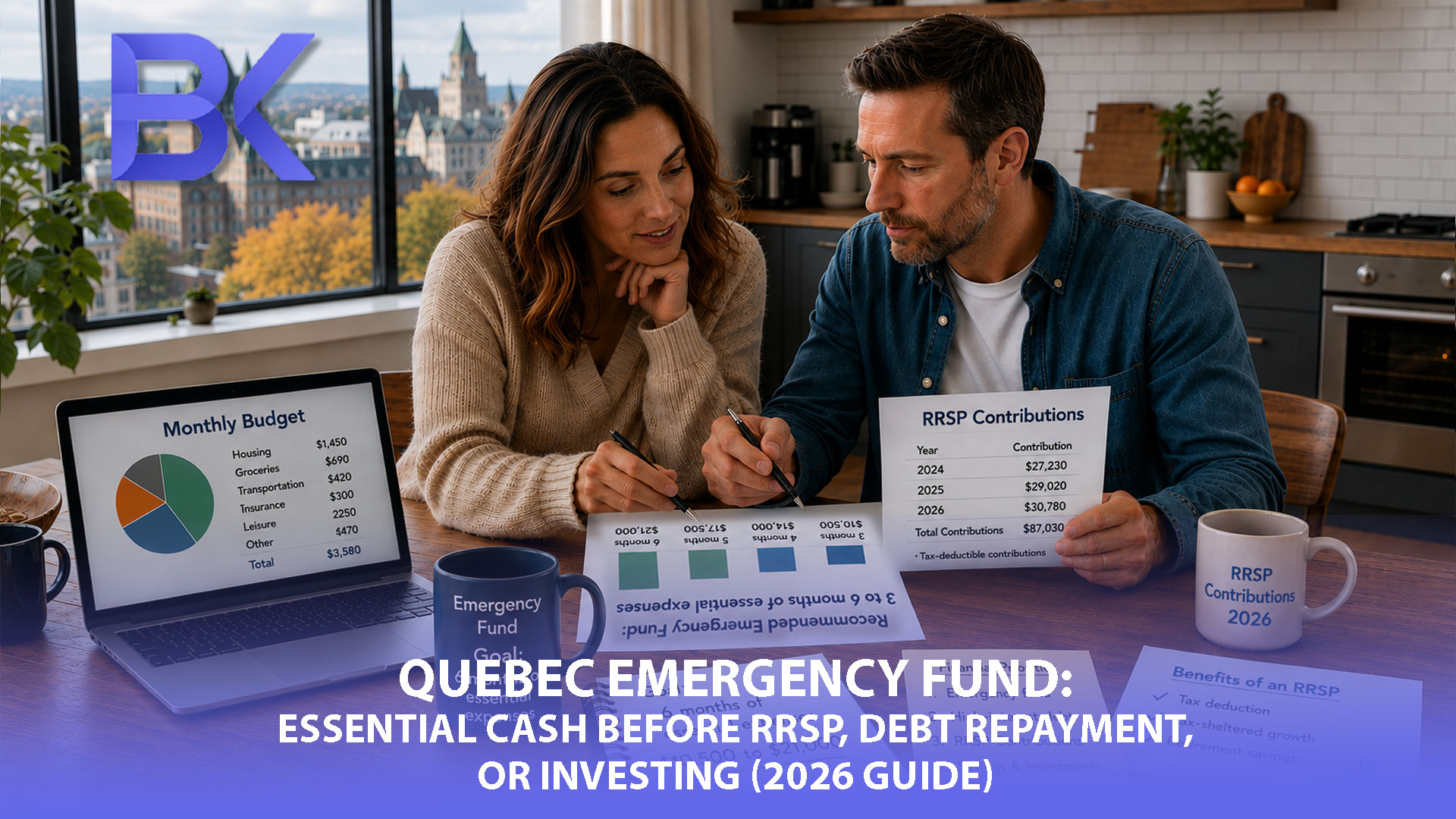

Calculating the Right Amount

Use net monthly essentials (after taxes and mandatory payroll deductions) when you calculate this figure; review bank statements for six months to confirm averages. Essentials include housing, food, insurance, minimum debt payments, and core family needs. Exclude dining out, vacations, and subscription services from this calculation. For variable income, self-employment, or new residency, 6 to 12 months may be more prudent.

Determine your monthly "must-pay" threshold. If your bare-bones essentials total $3,500 a month, your baseline emergency fund should be between $10,500 and $21,000.

Keep Emergency Cash Accessible, Not Invested

Emergency funds strictly belong in high-interest savings accounts or similar low-risk, liquid vehicles. They are not for market growth. If you invest your emergency fund in the stock market and a recession hits, market volatility can reduce the value of invested emergency savings just when you need cash; keep your emergency fund in liquid, low‑risk vehicles at the exact moment you lose your job and need the cash most.

| Household Situation | Suggested Emergency Fund | Main Reason |

| Dual stable income, low debt | 3 months | Lower income interruption risk |

| One income or variable pay | 4-6 months | Higher cash-flow pressure |

| Self-employed or newcomer | 6-12 months | High income uncertainty |

| Homeowner with older property | Add an extra $5K buffer | Unexpected repair surprises |

For an official budgeting tool and sample templates, see the FCAC budget planner and Canada.ca savings guidance.

RRSP Contributions vs. Emergency Fund

Quebec residents constantly debate whether to maximize RRSP contributions or build an emergency fund. The correct decision hinges on your current liquidity.

If you lack any cash reserve, establishing a "Starter Fund" of $2,000 to $5,000 must happen before you make significant RRSP contributions. This covers immediate, urgent needs (like a broken car or a dental emergency) without requiring a credit card.

Avoid Using an RRSP as Emergency Cash

An RRSP is completely unsuitable as an emergency fund. Withdrawals are heavily taxed immediately upon withdrawal, you permanently lose that contribution room, and it disrupts your long-term compounding growth. Immediate needs prioritize liquidity over tax deferral.

When RRSP Contributions Can Make Sense First

The only exception is if making an RRSP contribution generates a significant, guaranteed tax refund that you can then use to fully fund your emergency reserve. This "gross-up" strategy works well for Quebec professionals in high tax brackets, provided they don't spend the refund on a vacation.

Debt Repayment Priorities in Quebec

While aggressively paying down debt is important, it should not generally precede emergency savings entirely. If you throw every extra dollar at a credit card and have zero cash left, the next unexpected bill will force you to borrow on that exact same credit card again.

A balanced "Order of Operations" strategy is best:

- Starter Fund: Save $2,000 to $5,000 in cash immediately.

- Employer Match: Contribute just enough to your RRSP/pension to get any free money matched by your employer.

- High-Interest Debt: aggressively pay down credit cards and high-interest loans.

- Full Emergency Fund: Build up to your full 3-to-6-month cash reserve.

- Long-Term Investing: Maximize your TFSA, FHSA, and remaining RRSP room.

Net Income and Paycheck Reality

Your emergency fund must reflect your actual net income constraints. For Quebec employees, heavy deductions like provincial income tax, QPP, EI, and QPIP significantly reduce your disposable income. This explains why a seemingly high gross salary can still result in incredibly tight monthly cash flow.

Review your last 6 months of bank statements to find your true, consistent essential costs. Plan your emergency fund based on this hard data, not optimistic projections.

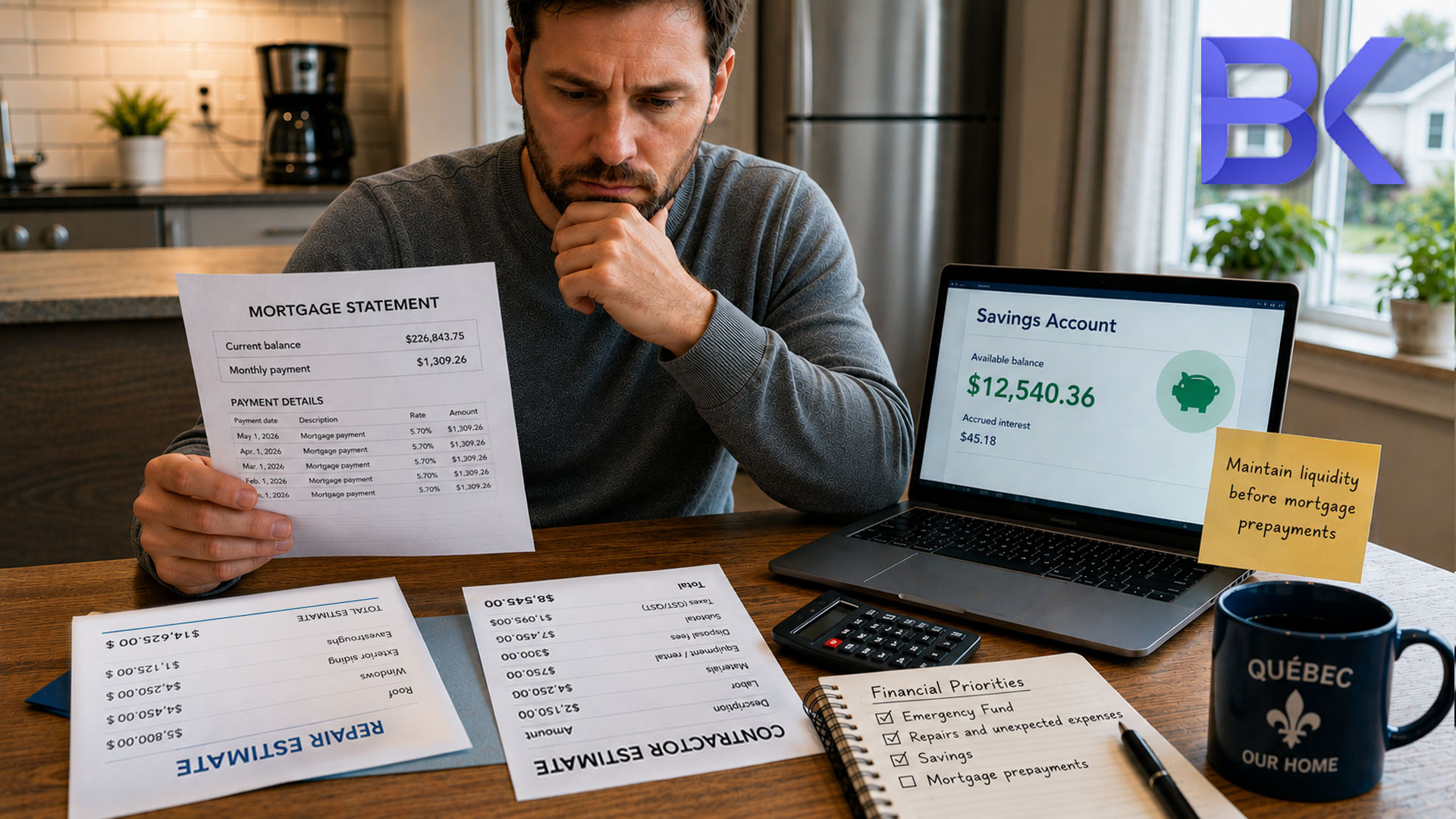

Mortgages and Emergency Cash Needs

Homeowners frequently question extra mortgage payments versus savings. In Quebec, homeownership dramatically increases your need for an emergency fund.

Mortgage payments are just the beginning. Property owners face municipal taxes, school taxes, insurance, heating, and sudden maintenance.

Before Making Mortgage Prepayments, Ask Yourself:

- Does my emergency fund cover 3 to 6 months of essentials?

- Can I afford a $10,000 roof or foundation repair without relying on a line of credit?

- Would a brief, two-month job loss jeopardize my mortgage payments?

If you are unsure, get a quick professional estimate (roof, foundation, heating) – conservative contingency planning reduces the chance of surprise borrowing.

Once your 6-month reserve is fully funded and your high-interest consumer debt is gone, then prepaying a mortgage becomes a fantastic, risk-free investment.

2 Real Cases: Emergency Funds in Action

Case 1: Montreal Couple Focused on the FHSA

A Montreal couple prioritized maxing out their FHSA and making extra mortgage payments, leaving them with only $1,500 in cash. Their essential monthly expenses were $4,200. When their car transmission failed, they had to put $4,000 on a high-interest credit card. The Fix: We paused their aggressive investing and built a $12,600 core reserve. They resumed their FHSA contributions three months later, but this time with zero financial stress and no reliance on credit cards for the next emergency.

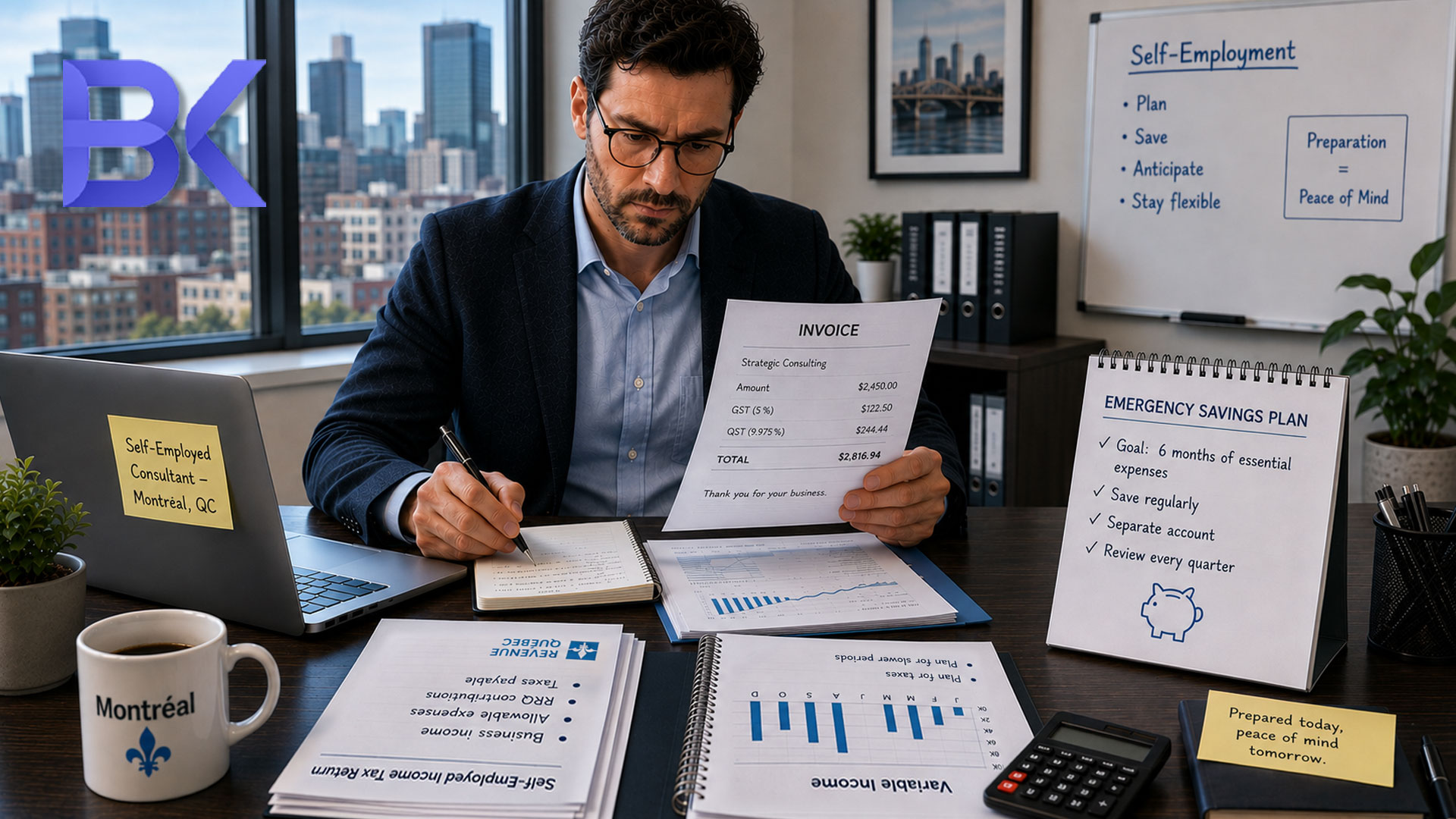

Case 2: Self-Employed Quebec Consultant

A self-employed consultant focused solely on debt reduction, throwing every invoice check at his line of credit. However, his fluctuating income led to constant re-borrowing during slower summer periods, creating a stressful cycle of debt. The Fix: By temporarily paying only the minimums on his debt, we built an 8-month emergency reserve and separated his tax funds into a different account. This stabilized his cash flow, permanently stopped the borrowing cycle, and allowed him to finally pay off the debt for good.

FAQ

How much emergency fund should I keep in Quebec before investing?

Aim for 3 to 6 months of essential living expenses. For those with irregular income, new homeowners, or self-employed individuals, 6 to 12 months is significantly safer.

Should I build an emergency fund before making RRSP contributions?

Yes. A starter fund of $2,000–$5,000 is strongly recommended as the minimum liquidity buffer before making larger, less-liquid contributions. The tax benefit of an RRSP never outweighs the massive financial risk of taking on high-interest credit card debt if an emergency strikes and you have zero cash.

Is it better to pay off debt or keep cash?

Build a starter emergency fund first, then aggressively target high-interest debt (like credit cards). Once the high-interest debt is gone, finish building your full 3-to-6-month emergency reserve. This strategy prevents you from being forced to re-borrow.

Where should I keep my emergency fund?

Use a highly liquid, low-risk account like a High-Interest Savings Account (HISA) or a cashable GIC. This fund must be immediately accessible and strictly separated from your daily checking account.

Does homeownership change the amount I need for an emergency fund?

Yes. Homeowners face significantly higher unexpected expenses (roof repairs, broken appliances, municipal tax hikes). Homeowners should carry a larger cash reserve than renters to buffer against these shocks.

Stop Living Paycheck to Paycheck with High Income

An emergency fund is not static; it evolves with life changes like homeownership, family growth, or employment shifts. Balancing cash security, debt reduction, and aggressive investing requires a tailored plan.

At BK Financial Services, Boris Kolodner, MBA, assists Quebec individuals, families, and businesses in creating highly practical financial plans that ensure every single dollar is allocated effectively.

Book Your Free Consultation Today for emergency fund check:

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

(Consultations available in English, French, Russian, and Hebrew. Secure your financial foundation today.)

Disclaimer: This article is provided for general informational and educational purposes only and should not be interpreted as individualized financial, investment, tax, legal, or accounting advice. Financial planning strategies should always be evaluated based on your personal financial situation, objectives, and risk tolerance. Consult a qualified financial professional before making major financial decisions regarding debt or investments.