With tax season officially behind us, many Quebec residents turn their focus to summer plans and completely overlook their Tax-Free Savings Account (TFSA). This is a costly mistake. Amid rising living costs, market volatility, and shifting financial goals, a flexible, tax-free savings vehicle is absolutely essential in 2026.

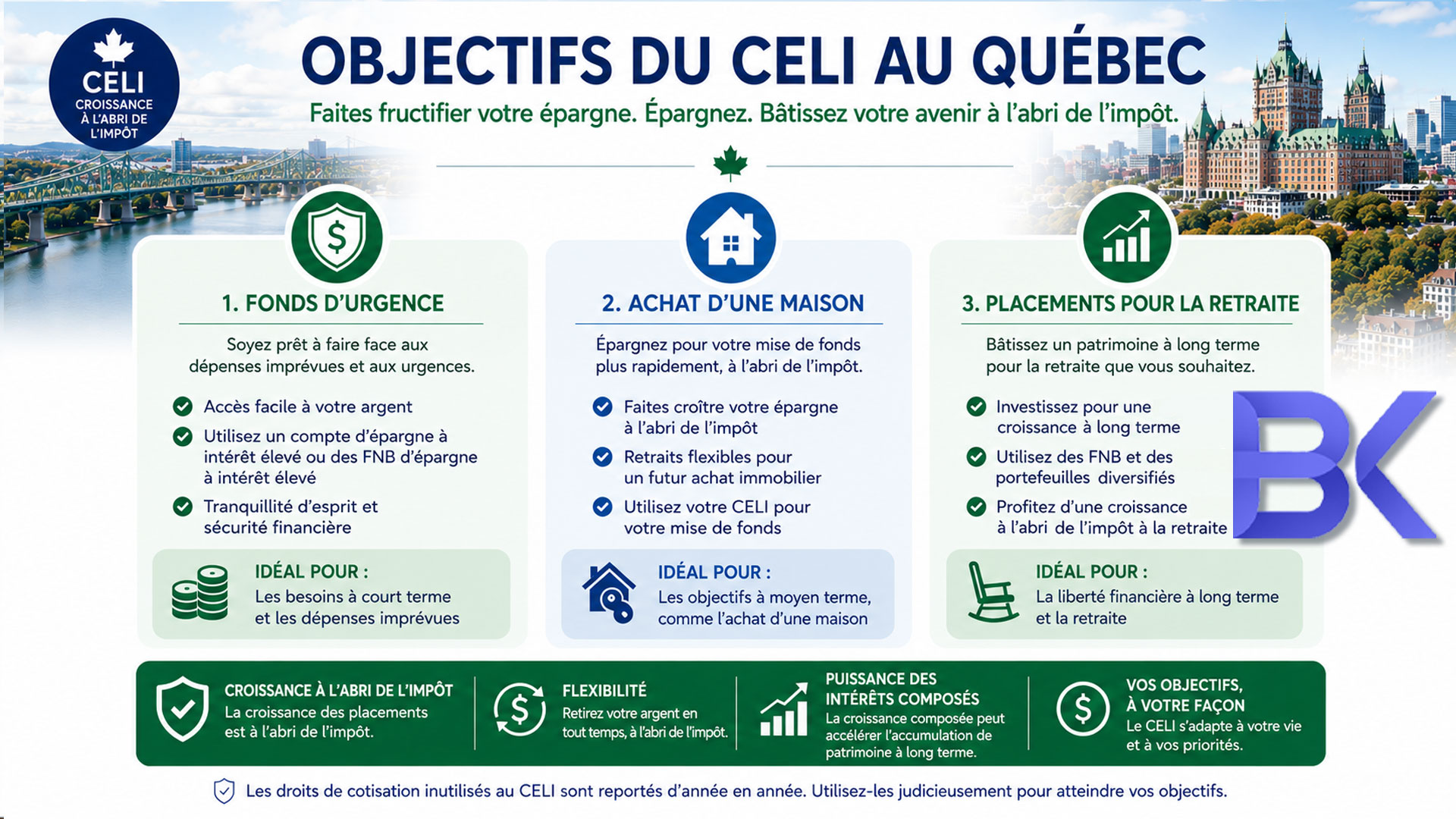

A properly managed TFSA can simultaneously act as your emergency fund, a down payment builder, and a tax-efficient retirement income source.

For Quebec individuals and families, a strategic TFSA approach enhances your net income planning without generating extra tax liabilities. This article reviews the 2026 TFSA contribution rules, investment considerations, and the most common, expensive mistakes Quebec residents must avoid this summer.

TFSA Contribution Limits for 2026

For 2026, the annual TFSA contribution limit is $7,000 (subject to CRA indexing and eligibility rules). However, your personal limit might be much higher. If you were 18 or older in 2009, have been a Canadian resident since then, and have never contributed to a TFSA, your cumulative available room in 2026 exceeds $90,000.

Reviewing your spring tax refunds and cash flow makes June the ideal time to plan your savings strategy.

Unlike an RRSP, a TFSA contribution does not reduce your taxable income. However, the incredible benefit is on the back end: all investment growth is tax-free, and withdrawals do not count as taxable income. This is crucial for Quebec retirees, as TFSA withdrawals will never trigger a clawback on your Old Age Security (OAS) or affect other income-tested benefits.

The #1 TFSA Mistake: The Re-Contribution Trap

The most frequent post-tax-season error involves misunderstanding the TFSA withdrawal rules.

Your available contribution room depends on your age, residency, past contributions, and past withdrawals. The Golden Rule: When you withdraw funds from your TFSA, that contribution room is not replenished immediately; it only returns to your limit on January 1 of the following calendar year.

Withdrawing funds in the spring to pay for a renovation, and then trying to recontribute that same money in the fall, can instantly trigger CRA overcontribution penalties. The CRA charges a punitive 1% tax per month on the highest excess amount in your account.

| TFSA Action | Tax Result | Critical Planning Note |

| Contribution | No tax deduction | Your money has already been taxed |

| Investment Growth | Completely Tax-Free | Perfect for long-term compounding |

| Withdrawal | Completely Tax-Free | Contribution room returns on January 1 of the next year |

Why Quebecers Need to Maximize the TFSA

Quebec features some of the highest marginal tax rates in North America. This makes sheltering interest, dividends, and capital gains particularly beneficial.

A TFSA is highly relevant for salaried employees receiving summer bonuses, self-employed individuals managing uneven cash flow, and retirees seeking to manage their taxable income. If you maximized your RRSP during tax season to get a refund, redirecting your monthly savings into a TFSA is the next logical step to build tax-free liquidity.

Stop Using Your TFSA as a Basic Savings Account

The name "Tax-Free Savings Account" is highly misleading. It should really be called a "Tax-Free Investment Account."

Many Quebec residents treat their TFSA like a basic bank account earning 1% interest. While this is acceptable for a short-term emergency fund, holding cash severely limits the long-term, tax-free compounding potential of the account.

A TFSA can hold various investments beyond cash. Depending on your risk tolerance, you can hold GICs, mutual funds, ETFs, stocks, and bonds inside a TFSA.

- Conservative TFSA (1-3 Year Horizon): Use cash or short-term GICs for funds needed soon (e.g., a home down payment or a wedding). This minimizes market risk but limits growth.

- Long-Term TFSA Portfolio (10+ Year Horizon): For retirement goals, a diversified ETF or professionally managed portfolio takes full advantage of tax-free compounding over decades.

| Financial Goal | Suitable TFSA Approach | Main Risk |

| Emergency Fund | High-Interest Savings Account (HISA) | Inflation eroding purchasing power |

| 1-3 Year Goal | Laddered GICs | Lower returns / Opportunity cost |

| 10+ Year Goal | Diversified ETF/Mutual Fund Mix | Short-term market volatility |

Retirement Planning Through a TFSA

The TFSA is becoming the most powerful tool for Quebec retirement planning.

For younger professionals, consistent post-tax-season contributions build massive future tax-free capital. For those nearing retirement, it perfectly complements your RRSP by offering withdrawal flexibility. Because TFSA withdrawals don't increase your net income, they support retirement cash flow without the massive tax impact of mandatory RRIF withdrawals in your 70s.

Other Costly TFSA Mistakes to Avoid

- Trusting Online Banking Balances Blindly: Do not assume your bank tracks your exact TFSA room in real-time. CRA reporting lags significantly. Always check your CRA "My Account" to confirm your room before making a large deposit, and track your current-year deposits manually.

- The "Transfer" Mistake: If you want to move your TFSA from Bank A to Bank B, you must request a direct institution-to-institution transfer. If you manually withdraw the cash from Bank A and deposit it into Bank B, the CRA considers it a new contribution, potentially triggering massive overcontribution penalties.

- Asset Location Mistakes: Placing highly taxed investments (like interest-bearing bonds) in non-registered accounts, while holding tax-preferred Canadian dividend stocks inside your TFSA, is inefficient. Your advisor should integrate your TFSA into a holistic "asset location" strategy.

2 Real Cases: BK Financial Experience

Case 1: Young Professional in Montreal Avoiding Penalties

- The Situation: A 31-year-old client wanted to deposit their massive $8,000 tax refund into a TFSA in June.

- The Problem: A quick review revealed they had already withdrawn $5,000 from the TFSA in February to buy a car, and only had $2,000 in unused room remaining for the current year. Depositing $8,000 would have triggered heavy CRA penalties.

- The Solution: We deposited $2,000 into the TFSA immediately. The remaining $6,000 was placed in a high-interest savings account and automatically scheduled for deposit the following January, safely avoiding all penalties.

Case 2: Self-employed Couple in Laval Shifting Strategies

- The Situation: A couple had maximized their RRSPs for years but lacked any flexible, accessible savings outside of their business accounts.

- The Solution: A post-tax-season review recommended pausing further RRSP contributions and focusing entirely on a TFSA strategy. We established an automatic monthly contribution plan. We used conservative GICs for a portion of the TFSA to serve as an accessible emergency fund, and diversified ETFs for the remainder to target tax-free retirement growth. This instantly improved their liquidity and reduced their financial stress.

FAQ

1. How much can I contribute to a TFSA in 2026?

The 2026 annual limit is $7,000. However, your total contribution room includes this $7,000, plus any unused room from previous years, plus any eligible withdrawals you made in 2025 or earlier.

2. Are TFSA withdrawals taxable in Quebec?

No. Qualified TFSA withdrawals are 100% tax-free and do not count as taxable income on your provincial or federal tax returns.

3. Can I recontribute the money I withdrew from my TFSA right away?

Only if you have enough unused contribution room available. Otherwise, the amount you withdrew is only added back to your contribution limit on January 1 of the following year.

4. What should I hold in my TFSA?

It depends on your timeline. Short-term emergency funds belong in HISA products or GICs; long-term retirement goals warrant diversified, growth-oriented investments like ETFs or mutual funds to maximize tax-free compounding.

5. Should Quebec residents prioritize a TFSA or an RRSP?

Not necessarily one over the other. RRSPs offer immediate tax deductions (great for high-income earners in Quebec), while TFSAs provide ultimate tax-free withdrawal flexibility. Most households benefit from a personalized strategy that uses both.

Stop Guessing with Your TFSA Strategy

A TFSA is a powerful wealth-building tool—but only when the contribution rules and investment strategies are coordinated properly. Don't risk expensive CRA overcontribution penalties or leave your money languishing in an account earning 1% interest.

At BK Financial Services, we help Quebec individuals, families, and self-employed professionals integrate TFSA planning with their RRSPs, FHSAs, mortgages, and broader financial goals.

Book Your Free Consultation Today:

- Phone: +1-514-834-5558

- Email: contact@bkfinancialservices.ca

- Website: https://bkfinancialservices.ca

(Consultations available in English, French, Russian, and Hebrew. Secure your financial peace of mind today.)

Disclaimer: This article is provided for general informational and educational purposes only and should not be interpreted as individualized financial, tax, investment, legal, or accounting advice. TFSA rules, contribution limits, CRA policies, and tax legislation are subject to change. Investment strategies should be evaluated based on your personal circumstances, time horizon, and risk tolerance. Consult a qualified financial professional before making financial decisions.